Accounting Conservatism Principle

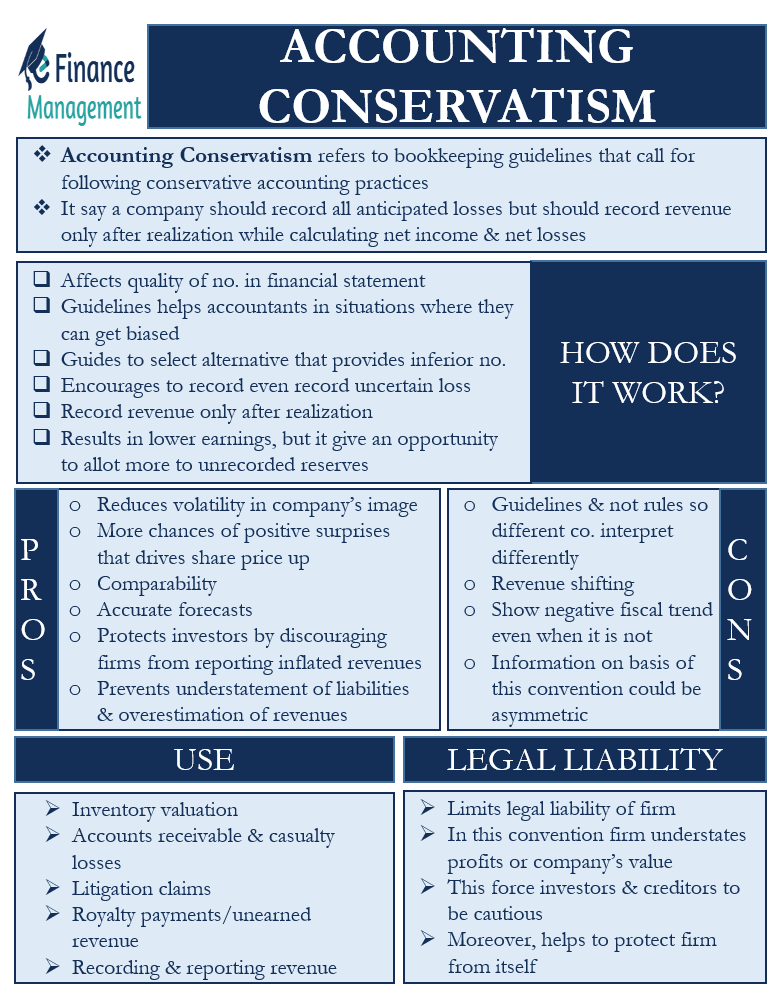

Accounting conservatism refers to the bookkeeping and accounting guidelines that call for following conservative accounting practices. These guidelines help firms avoid overestimating fiscal capacity or reporting the least aggressive numbers. For a firm following these guidelines, the standards to recognize the net income are much harder than for recognizing a net loss. For instance, under conservatism, the firm should only claim profits after fully verifying and realizing it.

Read more: Accounting Conservatism – Meaning, How it Works, Pros, Cons, and UsesIn simple words, we can say that conservatism means that the firm should take into account all worst-case scenarios when reporting its financial numbers. For instance, the firm should recognize all uncertain liabilities as soon as it discovers them. But, it should record the revenue only when they are sure about its realization. This accounting method wants the firms to select scenarios that give the most conservative income status. This indirectly makes the actual financial status stronger.

How does it Work?

Affects the Key Numbers

A company generally needs to follow several accounting conventions to ensure conveying its accurate financial numbers. Accounting conservatism is one of those conventions, and it requires accountants to take a cautious approach. This convention influences the quality and quantum of all the key numbers and key deliverables that are reported in the balance sheet, profit and loss account, and other financial statements.

Takes off the Individual Bias

A point to note is that conservatism does not lay down rules for the accurate reporting of numbers. Instead, it offers guidance to accountants when they face a situation where they need to estimate something using their judgment. So, we can say that conservatism helps accountants in situations where they can get biased. Or in other words, it tries to drive away the likely biases of the involved persons.

Also Read: Accounting Principles

Guides to Select Least favorable Number

Also, this convention lays down rules when an accountant faces two different alternatives. It must be noted that the conservatism convention does not tell the accountant which of the two alternatives he should select. Instead, this convention guides accountants to select the alternative that provides inferior numbers.

For instance, if it is not certain whether or not there will be a loss, then this convention encourages the accountant to record the loss. And, if an accountant faces a similar situation in case of a gain, then the convention encourages the accountant to ignore it until it materializes.

Revenue Recognition

For recognizing the revenue, this convention wants the accountant to ensure all information of a transaction is realizable before recording it. In case the transaction does not lead to any exchange of cash or any claim on an asset, then an accountant should not recognize the revenue.

This convention results in lower earnings, but it does allow the firm to allot more to the unrecorded reserves. Also, these unrecorded reserves give more flexibility to the firm to record higher earnings in the future.

Also Read: Accounting Information

Pros and Cons of Accounting Conservatism

Below are the pros of accounting conservatism:

- Since it guides a company to report lower net income, it ensures future financial advantages. Or, we can say it reduces the volatility in the company’s image.

- It encourages management to take more care when making a financial decision.

- There are more chances of positive surprises than of disappointing ones under conservatism.

- As most firms follow this convention, it makes it easier for investors to compare the numbers across periods and industries.

- It assists analysts in coming up with accurate forecasts.

- It protects investors by discouraging firms from reporting inflated revenues.

- This convention prevents understatement of liabilities and overestimation of revenues.

Following are the cons of this convention:

- Since this convention is only a set of guidelines and not rules, so different companies can interpret it differently. Thus, they can use it to their advantage or ignore it.

- It could result in revenue shifting. For instance, when recognizing revenue, if a transaction does not meet the requirements, it will not be reported in the current period. Instead, it would come in the future period. Such a treatment would understate the current period revenue and overstate the future period revenue.

- The numbers could show a negative fiscal trend even when there is not.

- The information based on this convention could be asymmetric.

Uses of Accounting Conservatism

Following are some of the most popular uses of conservatives:

- For inventory valuation, this principle suggests the accountant to use the lower of historical or replacement costs.

- Accountants also use this convention when estimating uncollectable account receivables (AR) and incidental losses.

- Even if a firm expects to win litigation, it should not report the gain from it until all revenue recognition principles are met. And, if a firm expects to lose the litigation claim, it must reveal its impact in the notes to the financial statements.

- Accountants should follow similar treatment (as above) in case of royalty payments or unearned revenue.

- This convention is also of use when recording and reporting revenue. Conservatives encourage accountants to match revenues and related expenses in the year they occur. Also, the convention discourages recording revenue if it is not realizable.

Legal Liability and Accounting Conservatism

Since this convention encourages firms to report worst-case scenarios, this, in turn, limits the legal liability of the firm. Due to conservatism, a firm understates its profits or understates the company’s value completely. This would force investors and creditors to be cautious, and this helps to limit the legal liability of the company.

Also, we can say that conservatism helps to protect a firm from itself. Since management gets conservative financial data, they make conservative choices. The rosy picture presentation would have prompted the management to take more risky decisions. Therefore, all such extra enthusiastic decisions are avoided.

Final Words

Accounting Conservatism is an important part of GAAP (Generally Accepted Accounting Principles). On the face, it may appear that this convention may not have many benefits as it overstates losses and understates profits. This could make the business unattractive to investors, at least on paper. In reality, this practice offers many distinct benefits to the business. The biggest is that it lowers the chances of unexpected (unpleasant) surprises. Moreover, it boosts the growth potential of the business.

RELATED POSTS

- Fundamentals of Accounting: Meaning, Principles, Categories, and Statements

- Accounting Policies – Meaning, Uses, Types, and Importance

- GAAP Accounting – All You Need To Know

- Management Accounting – Meaning, Definition, Tools, and Limitation

- What is Accounting?

- Difference between Financial and Management Accounting