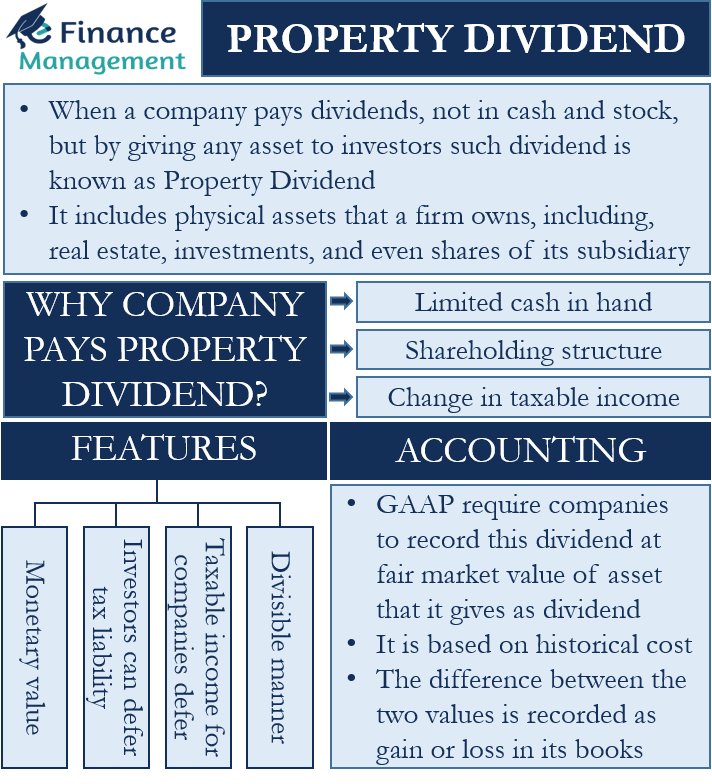

Understanding the Term: Property Dividend

When we talk about dividends, we assume it to be the dividend that a company pays in cash or stock. However, a company can pay non-cash dividends (other than stock) as well. And, if a company pays dividends, not in cash and stock, but by giving any asset to investors, we call such dividend a Property Dividend. We can also call this dividend as a Dividend in Kind.

For example, instead of giving dividends in cash, a company may give investors the products it sells. Such a type of dividend is not as common as a cash or stock dividend. This dividend could be for both – preferred or common stockholders. Though this type of dividend is uncommon, some companies do include a provision of this dividend option in the share issue agreement.

Property dividend usually includes physical assets that a firm owns, including, real estate, investments, and even shares of its subsidiary.

Why Company Pays Property Dividend?

There are mainly three reasons why a company may go for paying a dividend in such a way:

Limited Cash in Hand

A company may go for giving such a dividend when it does not have enough cash in hand. So by using a non-cash dividend, a company does not want to place any additional stress on its already starved cash flow.

Shareholding Structure

Another reason is if the company does not want to dilute its current shareholding. In that case, again the company issues property dividends rather than issuing additional stocks thereby increasing the liquidity and chances of stock grabbing by a few investors.

Taxable Income

A company may also go for this type of dividend if it wants to change its taxable income for avoiding profits. Since the asset that a company uses has to be revalued at the fair market value, it leads to loss or gains on the transaction.

Features

Following are the features of a property dividend:

Monetary Value

Even though such dividends are non-monetary, they do have a monetary value.

Deferred Tax for Investors

Such a dividend does allow investors to defer or lower their taxes. This is because an investor can hold onto it (the asset) for a longer time. And hence the incidence of tax is thus deferred till the disposal of the asset.

Taxable Income for Companies

Companies generally go for such a dividend if there is a significant difference between the fair market value and book value. This allows the company to change its taxable income.

Divisibility

The asset that the board decides to distribute as a dividend must be sufficiently divisible. Because like dividend it needs to be distributed to the shareholders in the ratio of their ownership. So before taking such a decision the company needs to ensure that the asset is divisible and distributable in such a manner. This is the reason why property dividend is mostly in the form of inventories and investments in securities rather than any fixed asset or real estate.

Accounting of Property Dividend

GAAP (Generally Accepted Accounting Principles) require companies to record this dividend at the fair market value of the asset that it gives as a dividend. As we know in line with the accounting practice the asset recording in books usually happens on a historical cost basis. Therefore, there is always a gap in the fair market value and the book value of the assets. So, the company records the difference between the two values as a gain or loss in its books.

Such an accounting treatment sometimes encourages a company to deliberately give property dividends as it helps to change the taxable income. And save it from tax incidence as well as cash flow issues. Hence the fair market value of the asset is taken in the books on the date of dividend declaration. A company can use different ways to arrive at a fair market value, such as using the market price of that asset, compared with a similar asset, or taking the help of an outside expert.

Property Dividend Journal Entry

The below example will clearly explain the accounting treatment of such a dividend.

Suppose Company A declares a dividend that it would pay in the form of shares of its subsidiary, Company B. The cost (face value) of these shares is $50,000, but their market value on the date of the declaration was $60,000.

Following will be the journal entries:

At the Time of Declaration

Shares Dr. $10,000 and Gain on Appreciation of Shares Cr. $10,000

Retained Earnings Dr. $60,000 and Property Dividends Payable Cr. $60,000

| Particulars | Dr. Amount | Cr. Amount | |

|---|---|---|---|

| Shares A/c | Dr. | $10,000 | |

| To Gain on Appreciation of Shares | $10,000 | ||

| (For gain in appreciation of shares) | |||

| Retained Earnings | Dr. | $60,000 | |

| To Property Dividends Payable | $60,000 | ||

| (For use of retained earnings to fund the dividend) |

At the Time of Distribution

Property Dividends Payable Dr. $60,000 and Investments in Company B Cr. 60,000

| Particulars | Dr. Amount | Cr. Amount | |

|---|---|---|---|

| Property Dividends Payable | Dr. | $60,000 | |

| To Investments in Company B | $60,000 | ||

| (For distribution of property dividend to shareholders) |

Final Words

A property dividend is not as popular as a cash or stock dividend. But they are an attractive option for both, the company and shareholders. Such a dividend allows a company to keep its cash reserves intact, not dilute its shareholding, and/or lower its tax liability. Similarly, it allows shareholders to defer or reduce their tax liability.