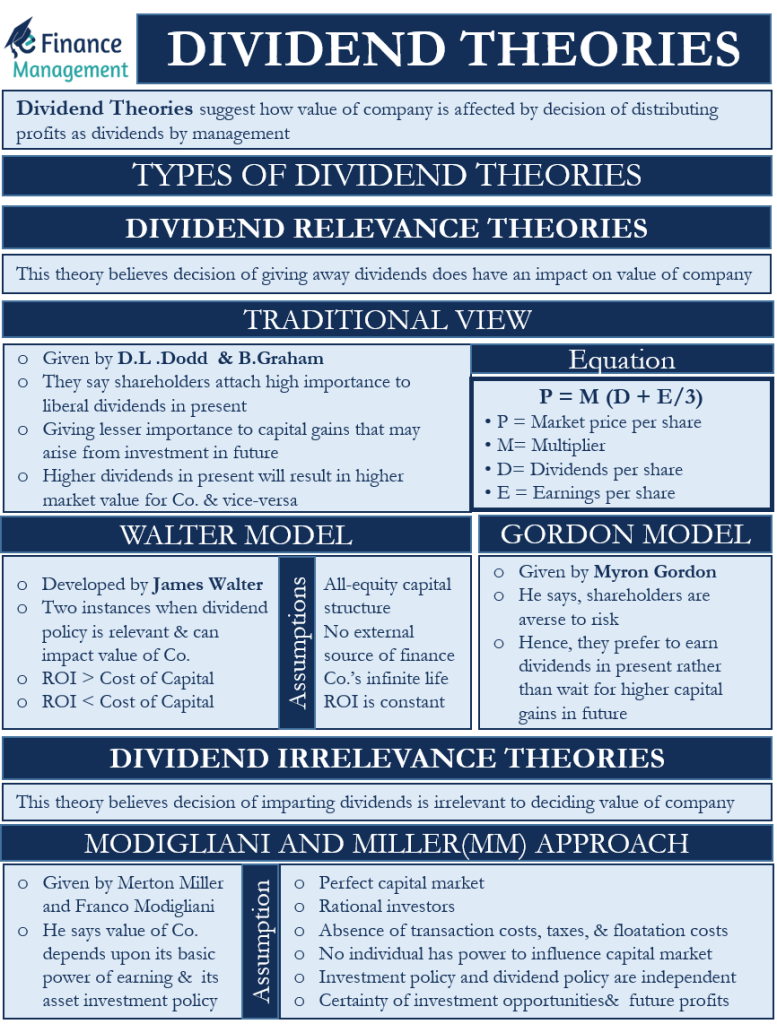

What are Dividend Theories?

A dividend is a reward for the shareholders of a company for investing in the company and continuing to be a part of it. Dividend distribution is a part of the financing decision for a company. The management has to decide what percentage of profits they shall give away as dividends over a period of time. They retain the balance for the internal use of the company in the future. It acts as an internal source of finance for the company. Dividend theories suggest how the value of the company is affected by the decision to distribute the profits as dividends by the management. It further affects on account of the frequency of dividend distribution and the quantum of dividend distribution over the years.

In the financing world, there are two types of theories that are most talked about. The first type is the Dividend relevance theory, according to which the decision to give away dividends does have an impact on the value of the company. The second type is the Dividend irrelevance theories that suggest that the decision to impart dividends is irrelevant to deciding the company’s share value and the value of the company.

Dividend Relevance Theories

There are three main types of Dividend Relevance Theories. Let us discuss those theories in some detail.

Traditional view

D.L.Dodd and B.Graham gave the Traditional view of dividend theory. According to them, shareholders attach high importance to liberal dividends in the present. They give lesser importance to capital gains that may arise from their investment in the future. In other words, the quantum of retained earnings has no relevance to the shareholders. Hence, higher dividends in the present will result in a higher market value for the company and vice-versa.

The Traditional view uses the following equation:

P= M (D + E/3)

Here, P= Market price per share, M= Multiplier, D= Dividends per share and E is for Earnings per share. E is the sum of Dividends (D) per share and the retained earnings per share (R). When we solve the equation, the weight that they attached to dividends (D) is four times the weight that they attached to retained earnings or E. This means that a liberal dividend policy has a favorable impact on the price of the stock and hence the valuation of the company.

Also Read: Walter's Theory on Dividend Policy

However, the above analysis is subjective. It does not have any practical justification and just represents the thinking of the two theory proponents.

Walter Model

The Walter model was developed by James Walter. According to him, the dividend policy is a relevant factor that affects the share price and value of the company. There are a few assumptions of the Walter model:

- The company has an all-equity capital structure.

- There is no external source of finance available to the company. The only source of finance for future investment projects is its internal source or its retained earnings.

- The company has an infinite life.

- The ROI is constant.

As per the model, there can be two instances when the dividend policy is relevant and can impact the value of the company. If the ROI or return on investment is greater than the company’s cost of capital, the shareholders would want the company to retain all of its earnings and avoid paying out any dividends. They will be better off if the company reinvests their earnings rather than investing them themselves. If the ROI is less than the company’s capital cost, the shareholders would want the company to pay out all of its earnings as dividends and not retain any amount. Because they feel that they can earn better returns than the company by investing in other available options.

However, in case the ROI is the same as the cost of capital of the company, the dividend policy will be irrelevant and will not have an impact on the value of the company. It will make no difference to the shareholders whether the company pays out dividends or retains its earnings.

Gordon model

The Gordon Model is the theory propounded by Myron Gordon. This model suggests that the dividend policy of a company is relevant and it does affect the market value of the company. Or understanding the dividend policy is necessary to arrive at the value of the company. According to him, shareholders are averse to risk. Hence, they prefer to earn dividends in the present rather than wait for higher capital gains in the future. This concept of present earnings is based on the age-old proverb – “A bird in the hand is better than two in the bush.” Therefore, this theory is also known as the bird in hand theory.

Also Read: Modigliani- Miller Theory on Dividend Policy

According to Gordon, dividends payout removes uncertainty from the minds of the investors. They care lesser about a higher income prospect in the future. Instead, they would want it now. Hence, dividends in the present will increase the value of the shares of the company and, eventually, its valuation.

Dividend Irrelevance Theories

Modigliani and Miller(MM) Approach

Merton Miller and Franco Modigliani gave a theory that suggests that dividend payout is irrelevant in arriving at the value of a company. Instead, the value of a company depends upon its basic power of earning and its asset investment policy.

The model makes the following assumptions:

- A Perfect capital market

- Rational investors

- Absence of transaction costs, taxes, and floatation costs.

- Information is freely available, and no individual has the power to influence the capital market.

- The investment policy and dividend policy of any company are independent of each other.

- There is a certainty of investment opportunities and future profits for a company.

According to the MM approach, a company will need to raise capital from external sources to make new investments when it pays off dividends from its earnings. Therefore, a gain in the value of the stock by paying off dividends is offset by a fall in the value of the stock due to additional external financing.

Therefore, this theory concludes that the dividend policy of the company is irrelevant to its market valuation. In other words, dividend distribution or non-distribution is of no importance to the investors or for the analysts to arrive at the value of the company. The valuation of the company will depend on other factors, such as expectations of future earnings of the company.

Summary: Dividend Theories

Both types of dividend theories rely upon several assumptions to suggest whether the dividend policy affects the value of a company or not. However, many of these assumptions do not stand in the real world. They have been used only to simplify the situation and the theory.

For example, suppose the management of a particular company decides to cut down on the dividend payout and retain more of its earnings. According to the Walter model, this happens when the internal ROI is greater than the cost of capital of the company. However, in reality, this may not mean that it has better use of the funds in hand and can provide a higher ROI than its cost of capital. The company may be going through a tough phase and needs more finance. Moreover, many assumptions in the above models, such as that of constant ROI, cost of capital and absence of taxes, transaction costs, and floatation costs, do not hold ground in the real world. A perfect capital market rarely exists, and investment opportunities, as well as future profits, can never be certain.

Thus, we should use these theories cautiously. We should use our judgment and not rely upon them completely to arrive at the value of the company and make investment decisions. All these should remain only reference points and not conclusive points.