Gordon’s theory on dividend policy is one of the dividend theories believing in the ‘relevance of dividends’ concept. It is also called the ‘Bird-in-the-hand’ theory, which states that the current dividends are important in determining the firm’s value. Gordon’s model is one of the most popular mathematical models to calculate the company’s market value using its dividend policy.

Crux of Gordon’s Model

Myron Gordon’s model explicitly relates the company’s market value to its dividend policy. The determinants of the market value of the share are the perpetual stream of future dividends to be paid, the cost of capital, and the expected annual growth rate of the company.

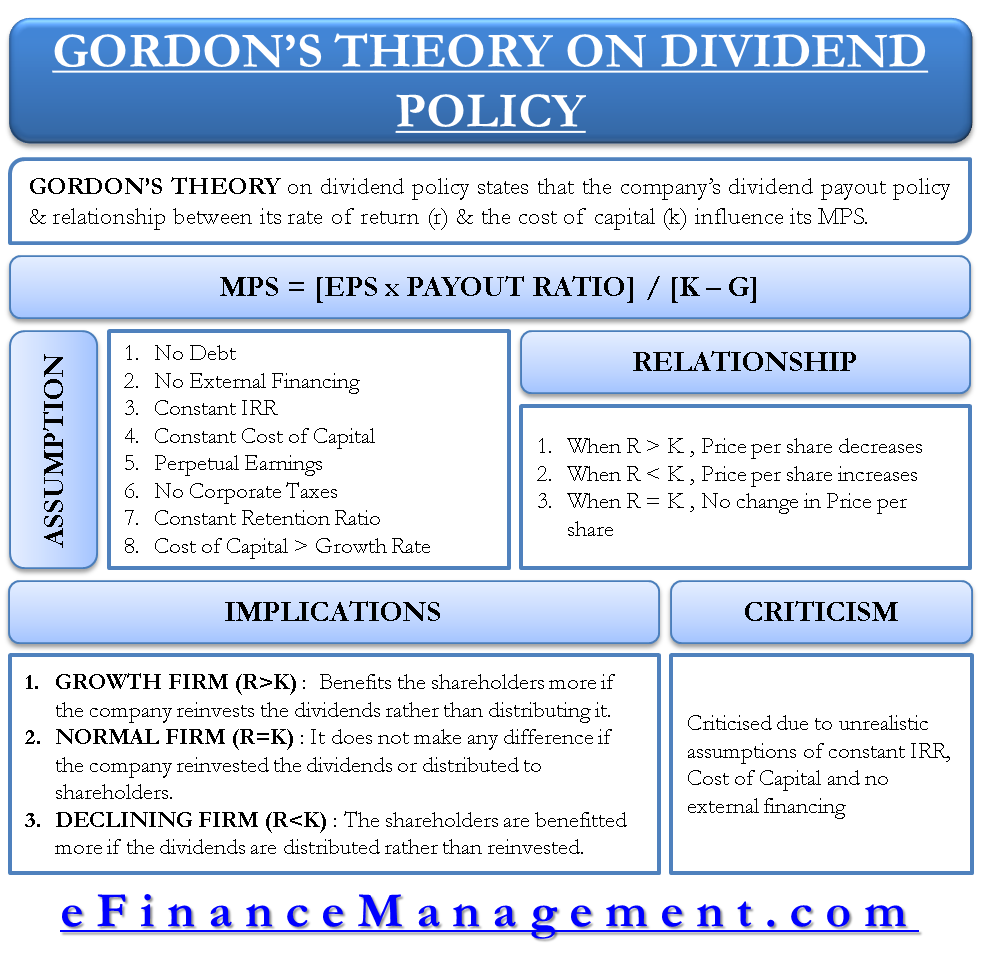

Gordon’s theory on dividend policy states that the company’s dividend payout policy and the relationship between its rate of return (r) and the cost of capital (k) influence the market price per share of the company.

Relationship between r and k

Increase in Dividend Payout

r>k

Price per share decreases

r<k

Price per share increases

r=k

No change in the price per share

Assumptions of Gordon’s Model

Gordon’s model is based on the following assumptions:

No Debt

The model assumes that the company is an all-equity company, with no proportion of debt in the capital structure.

No External Financing

The model assumes that retained earnings finance all investments of the company, and no external financing is required.

Constant IRR

The model assumes a constant Internal Rate of Return (r), ignoring the diminishing marginal efficiency of the investment.

Constant Cost of Capital

The model is based on the assumption of a constant cost of capital (k), implying the business risk of all the investments to be the same.

Gordon’s model believes in the theory of perpetual earnings for the company.

Corporate Taxes

This model does not account for corporate taxes.

Constant Retention Ratio

The model assumes a constant retention/plowback ratio (b) once it is decided by the company. Since the growth rate (g) = b*r, the growth rate is also constant by this logic.

k>g

Gordon’s model assumes that the cost of capital (k) > growth rate (g). This is important for obtaining the meaningful value of the company’s share.

Valuation Formula of Gordon’s Model and its Denotations

Gordon’s formula to calculate the market price per share (P) is P = {EPS * (1-b)} / (k-g)

Where,

P = market price per share

EPS = earnings per share

b= retention ratio of the firm

(1-b) = payout ratio of the firm

k = cost of capital of the firm

g = growth rate of the firm = b*r

Explanation

The above model indicates that the market value of the company’s share is the sum total of the present values of infinite future dividends to be declared. Gordon’s model can also be used to calculate the cost of equity if the market value is known and the future dividends can be forecasted.

The EPS of the company is Rs. 15. The market rate of discount applicable to the company is 12%. And it expects dividends to grow at 10% annually. The company retains 70% of its earnings. Calculate the market value of the share using Gordon’s model.

Market price of the share = P = {15 * (1-.70)} / (.12-.10) = 15*.30 / .02 = 225

Implications of Gordon’s Model

Gordon’s model believes that the dividend policy impacts the company in various scenarios as follows:

Growth Firm

A growth firm’s internal rate of return (r) > cost of capital (k). It benefits the shareholders more if the company reinvests the dividends rather than distributing them. So, the optimum payout ratio for growth firms is zero.

Normal Firm

A normal firm’s internal rate of return (r) = cost of the capital (k). So, it does not make any difference if the company reinvests the dividends or distributes them to its shareholders. So, there is no optimum dividend payout ratio for normal firms.

However, Gordon later revised this theory and stated that the firm’s dividend policy impacts the market value even when r=k. Investors will always prefer a share with more current dividend payments.

Declining Firm

The internal rate of return (r) < cost of the capital (k) in the declining firms. The shareholders will get more benefits if the company distributes the dividends rather than reinvesting them. So, the optimum dividend payout ratio for declining firms is 100%.

Criticism of Gordon’s Model

The main criticism of Gordon’s theory on dividend policy is due to unrealistic assumptions made in the model.

Constant Internal Rate of Return and Cost of Capital

The model is inaccurate in assuming that r and k always remain constant. A constant r means that the wealth of the shareholders is not optimized. A constant k means the business risks are not accounted for while valuing the firm.

No External Financing

Gordon’s belief that all investments being financed by retained earnings is faulty. This reflects the sub-optimum investment and dividend policies.

Conclusion

Gordon’s theory of dividend policy is one of the prominent theories in the company’s valuation. Though it comes with its limitations, it is a widely accepted model to determine the market price of the share using the forecasted dividends.

Sanjay Borad, Founder of eFinanceManagement, is a Management Consultant with 7 years of MNC experience and 11 years in Consultancy. He caters to clients with turnovers from 200 Million to 12,000 Million, including listed entities, and has vast industry experience in over 20 sectors. Additionally, he serves as a visiting faculty for Finance and Costing in MBA Colleges and CA, CMA Coaching Classes.

1 thought on “Gordon’s Theory on Dividend Policy”

in gorden d model of dividend theory, the assumption is “k >g ” why

in gorden d model of dividend theory, the assumption is “k >g ” why