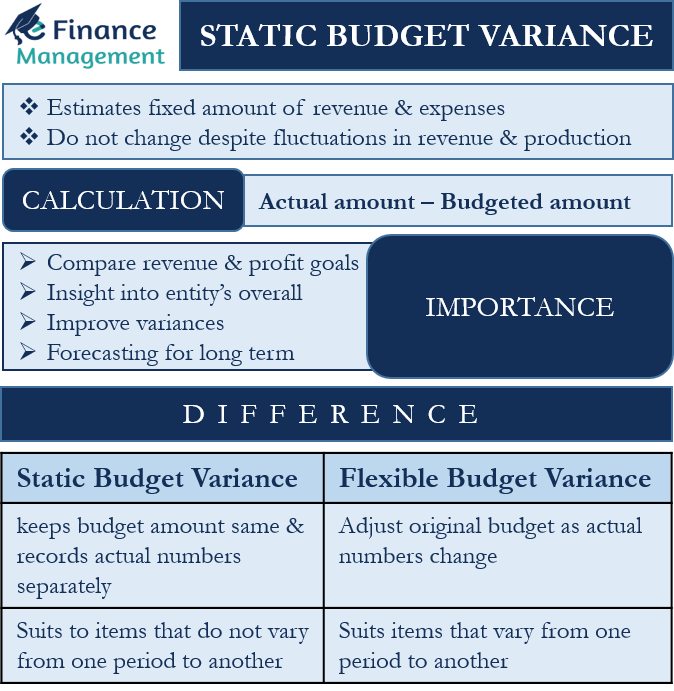

Understanding the term: Static Budget Variance

A static budget estimates a fixed amount of revenue and expenses. The budget figures in a static budget do not change despite the fluctuations in a company’s revenue or any other factors of production. Or, we can say that the actual performance of a period does not impact the budgeted numbers. Such a type of budget enables entities to allocate money to the items they expect to remain the same from one period to another. For example, rent or utility payments are common expenses that do not usually change from one year to another. However, like with any other budget, a static budget also has a variance, and we call this variance Static Budget Variance. Most simplistically, we can define the variance as the difference between the actual and budgeted numbers. Or any gap between the two numbers – actual and budgeted, is the Variance.

Importance/Uses of Static Budget Variance

A static budget variance arises when an entity compares the budget at the start of the term/period with the actual results at the end of the term/period. Analyzing this variance helps an entity compare its revenue and profit goals. It also gives management insight into its overall revenue performance and profit margin achievement.

Moreover, the variance can also help compare the static budget with any other type of budget. This regular comparison and variance analysis will further mature the budget planning system. And thus, the entity would be able to come up with an improved budget over the period that will ultimately seek to reduce the variances.

Another importance of the static budget variance is that it helps in forecasting for the long term. Forecasting for the short term is easy, but the accuracy drops when it comes to forecasting for the long term. This is where variance analysis helps. Understanding what one expected to happen and what happened over some time and could provide managers with relevant data and insight on how to minimize the variance.

Also Read: Flexible Budget Variance

How to Calculate Static Budget Variance?

To calculate the static budget variance, one needs to deduct the actual amount of each line item from the budgeted amount.

For example, the budgeted revenue is $5 million, and the actual revenue is $4 million. In this case, the variance will be $1 million. One can do the same for each line item or each component of the budget to come up with the variance for each item.

By this calculation or comparison, we get the variance in absolute terms. Alternatively, we can also calculate the variance in percentage terms. For this, we need to divide the absolute variance number by the budgeted number it represents. We need to divide $1 by $5 million in the above case. The variance will be 20%. Or, we can say that the actual sales were 20% less than the budget. And these variances can be favorable or unfavorable.

Managers must analyze both types of variances -positive and negative, for each line item to come up with meaningful information. To save time, the focus should be on variances that are well above or below expectations.

Static Budget Variance vs. Flexible Budget Variance

In a static budget, an entity keeps the budget amount as it is and keeps recording the actual numbers separately. And this difference between the original and the actual is what we call the variance. On the other hand, in a flexible budget, an entity would adjust the original budget as the actual numbers change. Flexible budget use percentages to set the amount.

Also Read: Variance Analysis

Another difference is that the static budget suits the items that do not tend to vary from one period to another. And flexible budget suits items that tend to vary from one period to another or are difficult to forecast.

For example, an entity’s static budget sets marketing expenses at $50,000. In case of a flexible budget, the marketing expenses will be 5% of sales. At the start of the year, both budgets will be at par. As the year progresses, the static budget will, in all probability will, create a variance. But the flexible budget will automatically adjust as the sales go up or down.

In the real world, most entities use both types of budgets. This is because the flexible budget assists the management in making real-time decisions based on the entity’s actual performance. And the static budget variance helps the management to find out why and where the actual performance was different from the budgeted one.

Final Words

Static Budget Variance may not provide real-time information on the performance of an entity. But, it does help the managers make their predictions accurate in the long term. Thus, an entity must not solely use a static budget but instead use it along with a flexible budget. A flexible budget will help with real-time data to make better decisions in a period, while a static budget will help to improve the accuracy of the budget.

RELATED POSTS

- Cost Variance – Meaning, Importance, Calculation and More

- Static Budget – Meaning, Importance, Benefits and More

- Fixed Budget – Meaning, Benefits, Drawbacks, and More

- Price Variance – Meaning, Calculation, Importance and More

- Variance Analysis Report

- Fixed Overhead Spending Variance – Meaning, Formula, Example, and More