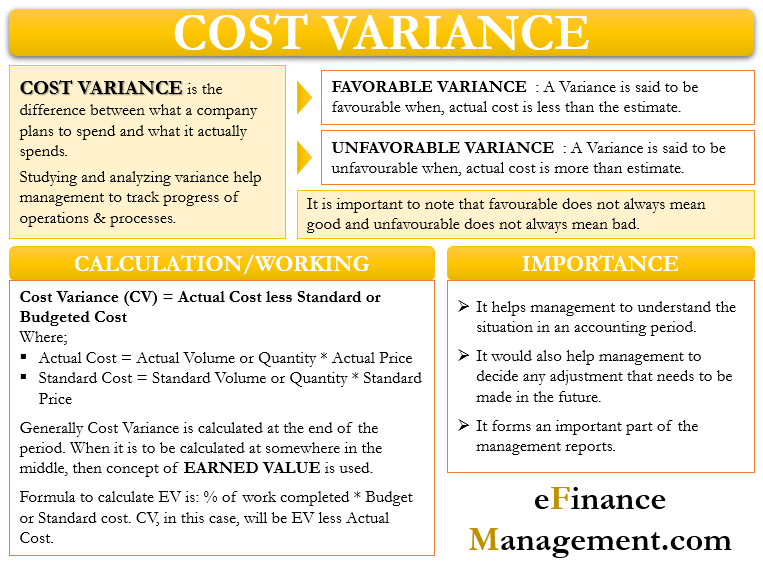

Cost Variance (CV) is a term that relates to the budget. As you will be aware, Variance is the difference between the cost and the estimates. Similarly, cost variance is the difference between the actual cost that a company incurs and the budgeted or estimated, or standard cost. In simple words, it is the difference between what a company plans to spend and what it actually spends. Management usually estimates the cost at the start of the accounting year.

They were studying and analyzing the variance to help the management to track the progress of the operations and processes. Usually, managers calculate CV for the expense line items. A company can use it to track a job or project as well, but there should be a standard or budget against which the actual job or project costs can be compared.

Some common cost variances are Labor rate variance, direct material price variance, purchase price variance, fixed overhead spending variance, and variable overhead spending variance.

Favorable or Unfavorable Cost Variance

A variance can be favorable or unfavorable. It is favorable if the actual cost is less than the estimate. And, it is unfavorable if the actual cost is more than the budgeted cost.

For example, Company A expects the labor cost for next year to be $500. But, due to inflation and shortage of labor, the actual labor cost was $700. The $200 difference is the cost variance. In this case, the variance is unfavorable.

A point to note is that an unfavorable variance is not always bad. Sometimes, it may happen that it becomes important for a company to spend more on some item for the company’s overall good. For example, a company may incur more on maintaining an asset to extend its useful life.

Similarly, a favorable variance may not always be good for a company. For example, a company may have got a favorable variance by spending less than necessary on customer service. This could have long-term consequences, and the company may lose clients.

Sometimes, it is better to analyze the cost variance keeping in view the department or full facility rather than at a granular level.

Calculating Cost Variance

To calculate the cost variance, it is important that the company comes up with the standard cost. The standard cost is nothing but a reasonable estimate or the cost that the company plans to incur in the period. The standard cost could be of anything, such as direct labor, direct materials, any overhead, or more.

After the company sets the standard costs for a period, it can start with the production process. Once the period ends, the company can go ahead and calculate the cost variance. The company does this by analyzing the actual costs and the standard costs that it set at the start of the period.

Also Read: Variance Analysis

The variance could be favorable or unfavorable. After identifying if the variance is favorable or unfavorable, the company can further break it down into components. A cost variance has two components – price and volume. Both these components also have standard and actual values. So, we will have the following equations:

Cost Variance (CV) = Actual Cost less Standard or Budgeted Cost

Actual Cost = Actual Volume or Quantity * Actual Price

Standard Cost = Standard Volume or Quantity * Standard Price

Cost Variance and EV (Earned Value)

The above formula is useful only when calculating the variance at the end of the period. Often cost accountants face a situation when they have to find a CV before the end of the period. In such a case, the concept of Earned Value (EV) comes useful. EV is basically the money that a company earns from work completed at a specific time.

Formula to calculate EV is: % of work completed * Budget or Standard cost

CV, in this case, will be EV less Actual Cost.

Let us take an example to understand the calculation using EV.

Company A is working on a project that they expect it to complete in 12 months. The total cost of the project is $100,000. After four months, the cost accountant determines that 30% of the project is complete and the company has spent $50,000.

EV in this case will be 30% * $100,000 or $30,000.

CV will be $30,000 less $50,000 or $20,000. This means Company A is over budget after four months, and it should take corrective actions.

Important note: One thing that is most important for calculating a CV is the budgeted or standard cost. If there is no reasonable foundation for the standard cost, then the variance won’t be significant as well.

Importance

The following points highlight the importance of a CV:

- The equations above can help management understand the situation in an accounting period. Also, it would help the management to decide on any adjustment that needs to be made in the future. For instance, once management knows the variance, it can use this variance to set standard costs for the next period.

- These variances also form an important part of the management reports.

- Some variances also serve as an input for the standard calculations, which provides in-depth insight into the given data.

- There could be two possibilities of a variance. One, it could be due to a human error, and second, due to an external factor, such as a supplier unable to deliver. Often these events are preventable with the help of risk management strategies.

Refer to Variance Analysis for more details.

Role of Cost Accountant

Generally, a cost accountant is responsible for tracing, investigating, and reporting the CV. Further, the cost accountant is also responsible for determining the reasons for the variance. The accountant then reports their findings to the management and a recommendation to lower the unfavorable variance or turn unfavorable to favorable variance.

In real life, there are more than one cost variances that a cost accountant comes across. However, they should not report all the variances to the management. Instead, in their report, the cost accountant should only talk about variances that they believe are significant or are large enough to get the attention of the management. The cost accountant may briefly talk about other smaller references in the report.

Final Words

Ideally, the budget and the actual cost should be equal, or the CV should be zero. But, this is not possible in the real world. Thus, the objective of a company should be to minimize the variance. A company that is able to keep its variance low can get success in controlling the risks as well.

Quiz on Cost Variance

This quiz will help you to take a quick test of what you have read here.

RELATED POSTS

- Material Variance

- Static Budget Variance – Meaning, Importance, and Calculation

- Production Volume Variance: Meaning, Formula, Limitations, and More

- Fixed Overhead Spending Variance – Meaning, Formula, Example, and More

- Variable Overhead Cost Variance – Meaning, Formula, and Example

- Variance Analysis Formula with Example

Nice, educative and impacting