Both operating and financial budgets are part of the master budget. While discussing differences between operating and financial budgets, first, let us understand what is a budget, an operating budget, and a financial budget. Let us see more about operating vs financial budget.

A budget simply means an expected forecast of income and expense for a specific period of time. Unquestionably, it is a very important management decision-making tool. Moreover, a budget is useful throughout the year in all the functional areas of an organization in giving directional guidance. Both an individual, as well as a large organization, prepare a budget in some form or the other.

An operating budget is a detailed statement showing all the operational expenses and incomes expected during a particular period of time. Therefore, an operating budget reveals how much profit an organization will generate given the assumption of revenues and expenses proves right in the future.

A financial budget is a financial plan which includes the receipts and payments incurred on a long-term and short-term basis. Basically, the focus here is to budget ‘Cash’ whether inflow or outflow.

Also Read: Types of Budget

Similarities: Operating vs Financial Budget

Let’s discuss some similarities between these two types of budgets – Operating and Financial.

- Both operating and financial budgets deal with future.

- These budgets contain the key information of the company.

- The basis of operating and financial budgets is past data and future assumptions.

- Both these budgets are expressed in financial value terms.

- They are a handy tool for management decision-making.

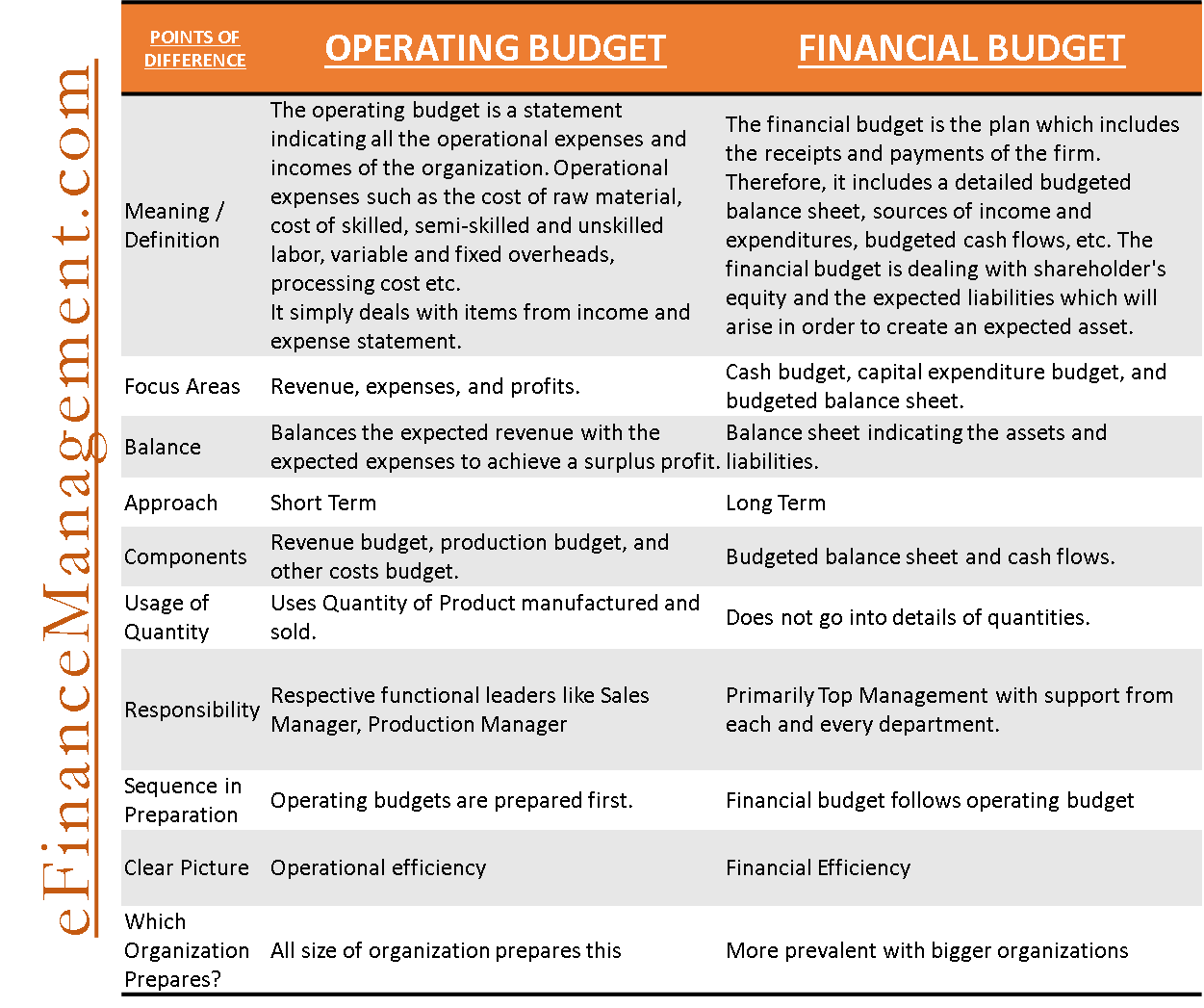

Difference between Operating Vs Financial Budget

| Points of Difference | Operating Budget | Financial Budget |

Meaning / Definition | The operating budget is a statement indicating all the operational expenses and incomes of the organization. Operational expenses such as the cost of raw material, cost of skilled, semi-skilled and unskilled labor, variable and fixed overheads, processing cost, etc.

It simply deals with items from income and expense statement. | The financial budget is the plan that includes the firm’s cash inflow and outflow. It includes a detailed budgeted balance sheet, sources of funds and capital expenditures, budgeted cash flows, etc. The financial budget deals with shareholders’ equity and the expected liabilities which will arise in order to create an expected asset. |

Focus Areas | An operating budget considers three major areas viz, revenue, expenses, and profits. | A financial budget considers cash budget, capital expenditure budget, and budgeted balance sheet. |

Balance | The operating budget balances the revenue from expected sources with the expected expenses. Accordingly, both the revenue and the expenses have to be aligned and there must be a surplus profit. | The financial budget includes the balance sheet indicating the assets and liabilities at any time during the year. It also has a linkage to the income and expenditure of the organization. |

Approach | As can be seen, the operating budget deals with the revenue and expenditure areas. Therefore, the approach is short-term. It helps the management in taking short-term decisions. | As financial budget deals with the cash budget, capital budgeting, and balance sheet. Therefore, the approach is long-term. It helps the management in taking long-term decisions. |

Components | The major components of the operating budget are revenue budget, production budget, and other costs budget. | The major components of the financial budget are the budgeted balance sheet and cash flows. |

Usage of Quantity | As can be seen, the operating budget requires more of quantitative detail for analysis. Production and sales budget requires planning the production of a number of units and the number of selling units, respectively. | The financial budget is prepared based on the expected receipts and the expected payments. Therefore, the financial budget avoids quantitative details. |

Responsibility | The successful implementation of the operating budget depends on the respective functional leaders. As an illustration, if the sales manager effectively manages sales, the budget seems easily achievable. On the contrary, if the production manager is not able to meet the production target, it becomes a bottleneck for the sales department. | Although the primary responsibility lies with top management, the successful implementation of the financial budget is dependent on all the departments. If any of the departments underperforms, there shall be a deviation in the financial budget. As an illustration, if the production departments overstock not obeying the budgets, and the sales department is not able to achieve the target sales. The overall finance cost shall go high. It is because working capital requirement will increase and therefore the cost. |

Frequency of Change | The operating budgets do not tend to change frequency. Not to mention, the sales and production targets are decided based on past trends and future market factors. Hence, it does not tend to change frequently. | The financial budget may need to change more frequently than the operating budget since it is affected by many external factors. The factors include but not limited to the prevailing rate of interest of borrowing, the foreign exchange rates, accounts receivables collection ratios. Therefore, the overall operating cycle affects the financial budgets of the organization. |

Sequence in Preparation | At first, the operating budgets are prepared. Therefore, these form the base for financial budgets. | Followed by the operating budget, the financial budget is prepared. The financial budget includes some important data from the operating budget. |

Clear Picture | The operating budget gives the blueprint of the business in the shorter run. Further, on the basis of operating budgets, the operational efficiency of the organization can be checked. However, an organization cannot depend on the operating budget for financial efficiency. | The financial budget gives a clear blueprint for the business in the long run. Furthermore, the operational and financial efficiency of the organization can be checked based on the financial budget analysis. |

Which Organization Prepares these Budgets? | From a small organization to a giant organization, all prepare the operating budget to improve productivity and growth. | However, small enterprises are less attentive to the financial budget. In general, a small organization prepares the financial plan for 1-2 years and a big organization prepares the financial plan for 8-10 years for maintaining the current and future infrastructure. |

Though the overall aim of both the budget is enhancing the productivity of the organization, by roles and functions both the budgets are different.

In conclusion, both financial budget and operating budget work parallel and have distinct usage. Both the operating budgets and financial budgets are interlinked. Hence, an organization cannot afford to avoid any of these budgets.

Also, read Master Budget

I approve of this article. Thank you.