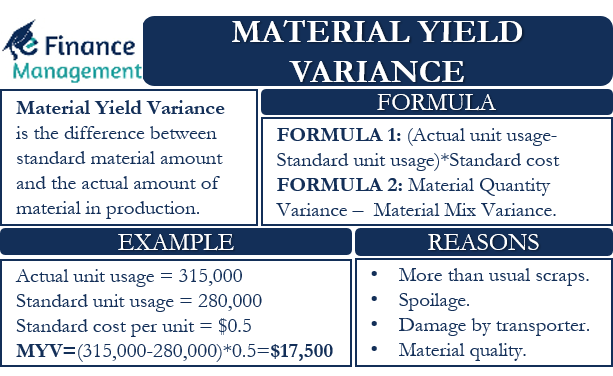

Material Yield Variance is the variance or the difference between the standard quantity of material consumption estimated and the actual amount of material consumed in production. And we multiply this difference with the standard cost of the materials to get the Material Yield Variance (MYV). In simple words, it’s a quantity variance of material converted to its cost to arrive at the monetary value of the variance. We can also call it Material Quantity Variance.

Usually, it is the engineering staff in a company that sets the standard for per unit of usage or consumption. Moreover, they consider several factors in setting standard unit usages, such as scrap rates, quality of materials, production process, and more.

MYV is a part of the material variances. One big difference between the MYV and other variance is that the calculation of other variance is on the basis of input, while MYV depends on the output.

Calculating MYV is very important in the processing industries, where the output from one process becomes the input of another. For such companies analyzing yield variance assists in maintaining control over the usage. All businesses would like to create an optimum output out of usage per unit of raw material. Hence, this variance is of quite importance.

Also Read: Material Variance

Reasons for Unfavorable Material Yield Variance

Like any other variance, MYV can also be favorable or unfavorable. However, it is primarily the unfavorable variance that a company needs to worry about. And an unfavorable variance occurs when the actual usage of material consumed is more than the standard usage. Following are the primary reasons for an unfavorable variance:

Scrap

When there is a change in machine setups, it may result in more than usual scraps. Scraps also increase in case of a change in acceptable tolerance levels or any change in the inspection process. So, the more scrap, the more the possibility and volume of variance.

Spoilage

Similar to scrap, an increase in spoilage may increase the chances of unfavorable variance. A company may witness spoilage because of any change in inventory and storage handling.

Damage by Transporter

There are always chances that the transport service is responsible for shipping the damages of the materials in transit. This may result in a variance.

Also Read: Variance Analysis Formula with Example

Material Quality

If the quality of material degrades, or the company starts procuring low quality, it would also increase the unfavorable variance.

Formula and Example of Material Yield Variance

Following is the formula that we use to calculate the Material Yield Variance:

(Actual unit usage less Standard unit usage) * Standard cost per unit

Now, let’s consider an example to understand the calculation of MYV.

Company A makes plastic desks and estimates that it needs 8 kg of plastic to produce one desk. In a year, Company A uses 315,000 kg of plastic to create 35,000 desks or 9 kg to produce one desk. The standard cost of one kg of plastic is $0.50.

The standard unit usage will be 8 kg * 35,000 desks or 280,000 kgs.

Putting the values in the formula: (315,000 less 280,000) * $0.50 = $17,500 Material yield variance. This variance is unfavorable because Company A uses more than the standard usage.

Another Formula for Material Yield Variance

Since MYV is a part of the material variance, we can also calculate the MYV by subtracting the material mix variance from the material quantity variance. The equation, in this case, will be MYV = Material Quantity Variance less Material Mix Variance.

The Formula to calculate Material Quantity Variance = (Actual quantity used × Standard rate) – (Standard quantity allowed/estimated × Standard rate).

This formula will be used for each type of material involved in the production. So we will come out with the quantity variance for each type of material.

OR

Standard Price [(Standard Quantity of one type of material/ (total standard material – Abnormal Loss)] X (Actual output – Actual Quantity)

The formula of Material Mix Variance = Standard cost of standard mix less Standard cost of the actual mix.

Example

Let us see an example to understand the calculation. For the sake of simplicity, in our example, we have kept the standard mix and actual mix of material the same.

Company A determines the following standard mix of materials X and Y to produce Z.

The standard mix is 200 units of X at the rate of $12 and 100 units of Y at the rate of $10.

The actual mix is 160 units of X at the rate of $13 and 140 units of Y at the rate of $10.

If the actual output is 275 units of Z and the standard loss is 10%, calculate the MYV.

As a first step, we need to calculate the Material Quantity variance (MQV)

MQV for X = $12 * (200/270) X (275-160) = $524.44. This variance is favorable.

MQV for Y = $10 * (100/270) X (275 -140) = $381.48. This variance is unfavorable

Net MQV = $524.44 less $381.48 = $142.96 favorable

Now, we need to calculate the Material Mix Variance (MMV).

Putting values in the MMV formula, we get:

Cost of Standard Mix = (200* $12+100* $10) = $3400

Cost of Actual Mix = ($12 *160) + ($10 * 140) = 3320

Thus, MMV is $80 favorable = $3400 – $ 3320.

Now, to calculate the MYV, we need to subtract Material Mix Variance from the material quantity variance.

Material Yield Variance = $142.96 less $80 = $62.96 favorable

Alternate Solution

Another method to arrive at MYV is as follows:

| Product | Standard Data | Actual Data |

|---|---|---|

| X | 200 Units | 160 Units |

| Y | 100 Units | 140 Units |

| Total Input | 300 Units | 300 Units |

| Standard/Actual Loss | 30 Units (i.e. 10%) | 25 Units (Balancing Figure) |

| Total Output | 270 Units | 275 Units |

With the help of the above table, we can calculate the standard input required for the output of 275 units.

Standard Input = 275 * 300 / 270 = 305.56

Now, we will divide this standard input in the ratio of 2:1 to arrive at the quantity of product X and product Y

- Product X = 203.71

- Product Y = 101.85

Therefore, material yield variance (using the formula)

- Product X = (203.71-200)*$12 = $44.47 Favorable

- Product Y = (101.85-100)*$10 = $18.49 Favorable

Total MYV = $62.96 Favorable

Verification of the Result

We can also verify this answer. To do this, we need to calculate the MYV using the direct formula, and the answer from both approaches should be the same.

To calculate MYV using the direct formula, we first need to calculate the Standard Mix for both X and Y.

For X = 200 units * $12 = $2,400

For Y = 100 units * $10 = $1,000

Total standard units after 10% loss will be 270 (300 less 10%).

Now we need to calculate the Actual Mix:

Material X = 160 units *$13 = $2,080

Material Y = 140 units * $10 = $1,400

The actual output is 275 units (after 10% standard loss).

Now, we need to calculate the Standard Cost per unit, and it is = $3400 / 270 = $12.593

Now putting the values in the MYV formula = $12.593 * (275 less 270) = $ 62.965 Favorable

So, the answer in both the cases is same. This means the calculations are accurate.

Final Words

A Material Yield Variance is a crucial metric that helps management determine the efficiency of the output. This metric, however, fails to tell the reason for the variance. So, it is important for a company to carry out a thorough analysis to determine the cause of the variance.

Refer to Material Variance for learning about other types of material cost variances.

Frequently Asked Questions (FAQs)

Material Yield Variance is the variance or the difference between the standard amount of material and the actual amount of material consumed in production multiplied by the standard cost of the material.

The 2 formulas for calculating material yield variance are:

Formula 1: (Actual unit usage less Standard unit usage) * Standard cost per unit

Formula 2: Material Quantity Variance less Material Mix Variance.

The reasons for the occurrence of material yield variance are:

1. Scraps

2. Spoilage

3. Damage by a transporter

4. Material quality

RELATED POSTS

- Direct Materials Quantity / Usage / Volume Variance

- Material Price Variance Calculator

- Material Mix Variance – Meaning, Example, and More

- Price Variance – Meaning, Calculation, Importance and More

- Cost Variance – Meaning, Importance, Calculation and More

- Production Volume Variance: Meaning, Formula, Limitations, and More