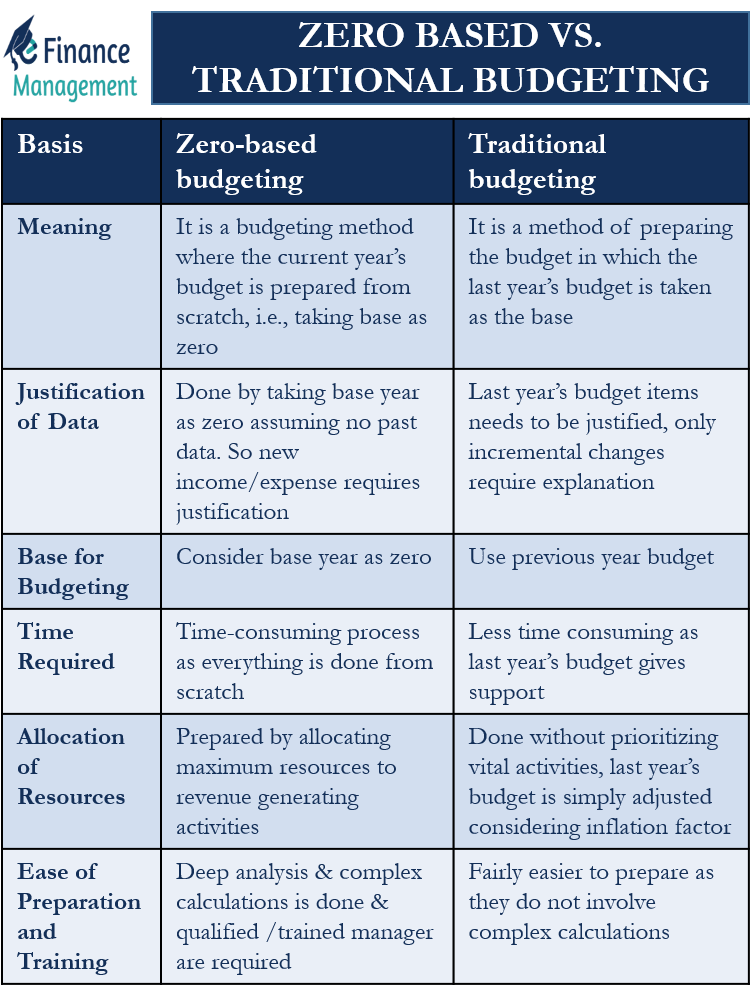

Zero-Based budgeting and traditional budgeting are the two predominantly used budgeting techniques. These techniques help the companies to allocate capital to different departments. These budgeting methods vary from each other in many aspects, viz. justification of data, the base of budgeting, ease in the modification of budget components, the time required, allocation of resources, ease of preparation and training, etc.

Both the methods have their own advantages and disadvantages. So companies need to wisely choose the preferred method choice, depending on what they desire to achieve through the budgeting process. Before going through the difference between zero-based and traditional budgeting, let us briefly understand their meaning.

Zero-based budgeting is a budgeting method where the current year’s budget is prepared from scratch, i.e., taking the base as zero. The old and the new activities of the business are ranked according to their importance. Based on that, resources are allocated to each activity without considering the past budgets or achievements.

Traditional budgeting is a method of preparing the budget in which the last year’s budget is taken as the base. The current year’s budget is prepared by making changes to the previous year’s budget by adjusting the expenses based on the inflation rate, consumer demand, market situation, etc. While preparing the traditional budgets, the past year’s revenues and costs form an integral part of the current year’s budget, as the current year’s budget is prepared by taking them as the base.

Also Read: Zero Based Vs. Incremental Budgeting

Zero Based Vs. Traditional Budgeting

The following points will highlight the points of difference between zero-based budgeting and traditional budgeting.

Justification of Data

Zero-based budgeting is done by taking the base as zero as if there is no past or historical data. Here all the items in the cash flow need to be justified. So a new expense or income and an old expense or income require a justification. While preparing the traditional budgets, only the items over and above the last year’s budget need to be justified. So, only incremental changes require an explanation, not everything else.

Base for Budgeting

Zero-based budgeting is done considering the base as zero (without considering the previous year’s budget). For every financial period, a fresh budget is prepared from scratch. On the other hand, traditional budgeting uses the previous year’s budget as a baseline to make the current year’s budget. So the main stress lies on the previous level of expenditure. Ease of Modification of Budget Components

In the case of zero-based budgeting, it is easy to eliminate an existing item or add a new item to the current budget, as zero-based budgeting is a creation of an entirely new budget from the ground. In other words, zero-based budgeting is more flexible in nature. The same is not the case with traditional budgeting. In traditional budgeting, it isn’t easy to modify budget components. Moreover, every year’s budget components are not exactly the same. Budget components change depending on the market conditions and the company’s objectives. Since traditional budgeting depends on the preceding year’s budget, it is not necessary that the company uses the same budget components as it used in the preceding year’s budget. Hence it is very difficult to modify or eliminate an existing item or add a new item to the current budget. In other words, traditional budgeting is comparatively rigid in nature.

Time Required

One of the biggest problems with zero-based budgeting is that it is a time-consuming process as the budget is prepared right from the start. Before being added to the budget, any project goes through a lot of comparisons and approvals, which leads to spending excessive time on each project. On the other hand, traditional budgeting is less time-consuming. Since changes are done in the previous year’s budget to meet the needs of the current period, half the work is already done before the budget process starts, and only incremental changes are required.

Allocation of Resources

In zero-based budgeting, the budgets are prepared by allocating maximum resources to those activities which benefit the organization. The activities that are revenue-generating and critical to the business’s survival get the topmost priority. So with zero-based budgeting, the management can focus on priority decisions. Traditional budgeting is done without prioritizing vital activities of the business, and last year’s budget is simply adjusted considering the inflation factor.

Ease of Preparation and Training

Zero-based budgeting requires justification for allocating available resources, which can be known only after deep analysis and complex calculations. Managers require special skills and knowledge to prepare zero-based budgets. Only a qualified and well-trained professional can prepare such budgets. Thus, the preparation of zero-based budgets is a complex task. Whereas traditional budgets are fairly easier to prepare as they do not involve complex calculations.

Quiz on Zero Based Vs. Traditional Budgeting

This helped alot