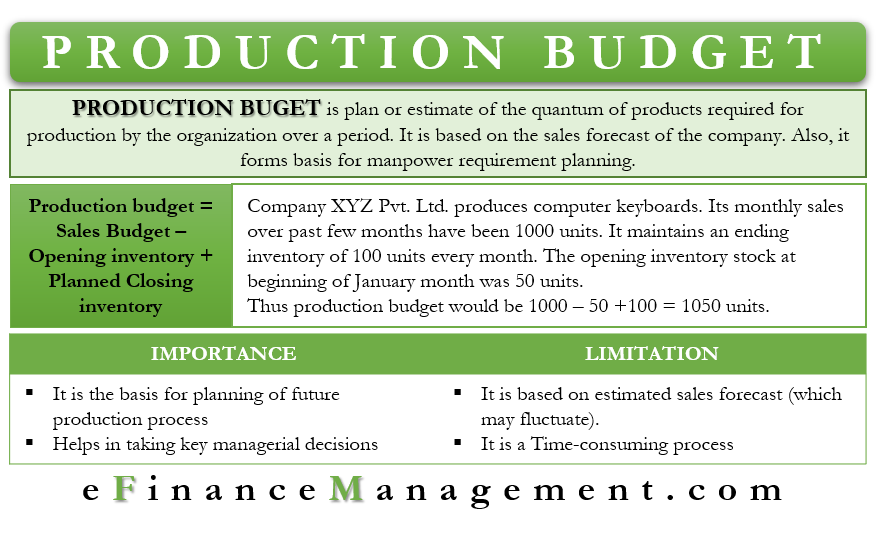

What is the Production Budget?

A budget is a financial plan for a defined period, whether monthly, quarterly or annually. It estimates a wide variety of parameters like sales, revenue, expenditure, etc., and is an essential exercise for every financial organization. The production budget is a plan or estimate of the quantum of products required for production by the organization over a period. It is an estimate based on the sales forecast, or how much the company will sell in the coming period. It also considers the desired inventory level the company wants to maintain to meet contingencies and avoid stock-outs.

The production budget is the basis for developing cost budgets about the raw materials and other consumables to be purchased. It is a type of operating budget. Also, it forms the basis for deciding how much manpower to be employed. Other important managerial decisions like the need and quantum of advertising and promotions, purchasing or taking storage spaces or godowns on rent, etc., are based upon the number of items to be produced.

How is the Production Budget Fixed?

The basis for preparing the production budget is the sales budget. How much the company can sell is directly dependent upon how much it produces. Also, the amount of inventory in the beginning and the inventory the company wants to keep with it at the end of the production cycle determines the production budget.

Therefore, in simple equation form, production budget = The sales budget or forecast + Planned inventory to be maintained in the end – Inventory in the beginning.

Also Read: Operating Budget

The above three factors are internal to any organization. Too much inventory balance, in the end, will result in the blocking of capital as well as storage space. Also, there is a risk of products getting obsolete or out of fashion, and the company may have to sell at a steep discount or loss. On the other hand, maintaining fewer inventories may result in stock-outs and loss of sales opportunities in case of a sudden surge in demand. Therefore, it is an uphill task to decide the amount of inventory to maintain in the end.

There are some critical external factors too that affect the production budget. These factors are the prevailing economic conditions, competition in the market, availability of substitutes, etc. A change in any of these external factors may directly affect the sales of the company, which in turn will affect the production budget. Therefore, these are important factors for consideration while preparing or analyzing a budget.

Example

Let us take an example of the company XYZ Pvt. Ltd., which produces computer keyboards. Over the past few months, its monthly sales have been 1000 units on average. It maintains an ending inventory of 100 units every month as a policy. The opening inventory stock at the beginning of January month was 50 units.

We will make use of the equation for the production budget to find out the optimum quantity the company should produce.

Production Budget= 1000 units (Sales forecast) + 100 units (Desired closing inventory) – 50 units (Inventory at the beginning)

= 1050 units.

Hence, the company has to produce 1050 units of the keyboard in January to meet its sales forecast and maintain an opening stock of 100 units at the beginning of February. The production budget for February should be:

Also Read: Sales Budget

= 1000 units (Sales forecast) + 100 units (Desired inventory at the end) – 100 units (Inventory at the beginning)

= 1000 units of keyboards.

Types of Production Budgets

Production budgets include:

- Direct materials budget

- Direct labor budget

- Production overhead budget

Importance of Production Budget

Basis for Planning of Future Production Process

A well-conceived production budget forms the basis for planning in any organization. The budget indicates the number of units to make. Hence, it does not take into account the cost of production. Thus, it helps to streamline the production process, machinery utilization, and proper scheduling of the same.

Helps in Taking Key Managerial Decisions

The production budget is the key to the purchase budget for the management. The purchasing of raw materials and consumables depends entirely on the production budget. Also, many other key decisions, like the recruitment of new personnel, depend upon how much production the company will do.

Limitations of Production Budget

Based on Estimates

This budget is based entirely on estimated values of sales. Also, maintaining inventory is subjective, with the possibility of a lot of variation. These figures are based on the management’s judgment. It can go wrong in unforeseen circumstances such as fluctuation in demand for the product or the supply of raw materials, changes in the economic situation, recession, or even due to competition.

Time-consuming Process

Preparing this budget is a lengthy process. Hence, It can consume a lot of time. In case estimates go wrong, it will result in the wastage of precious working hours.

Though there are some limitations with the budgets, budgets are still the guiding force for future action. Moreover, all budgets reflect the estimation or plan for the period and are based on certain assumptions.