A non-deliverable forward contract is a type of forward contract used to hedge foreign exchange risk. Some of the other foreign exchange risk hedging instruments are currency futures, currency options, and currency swaps.

Definition of Non-deliverable forward

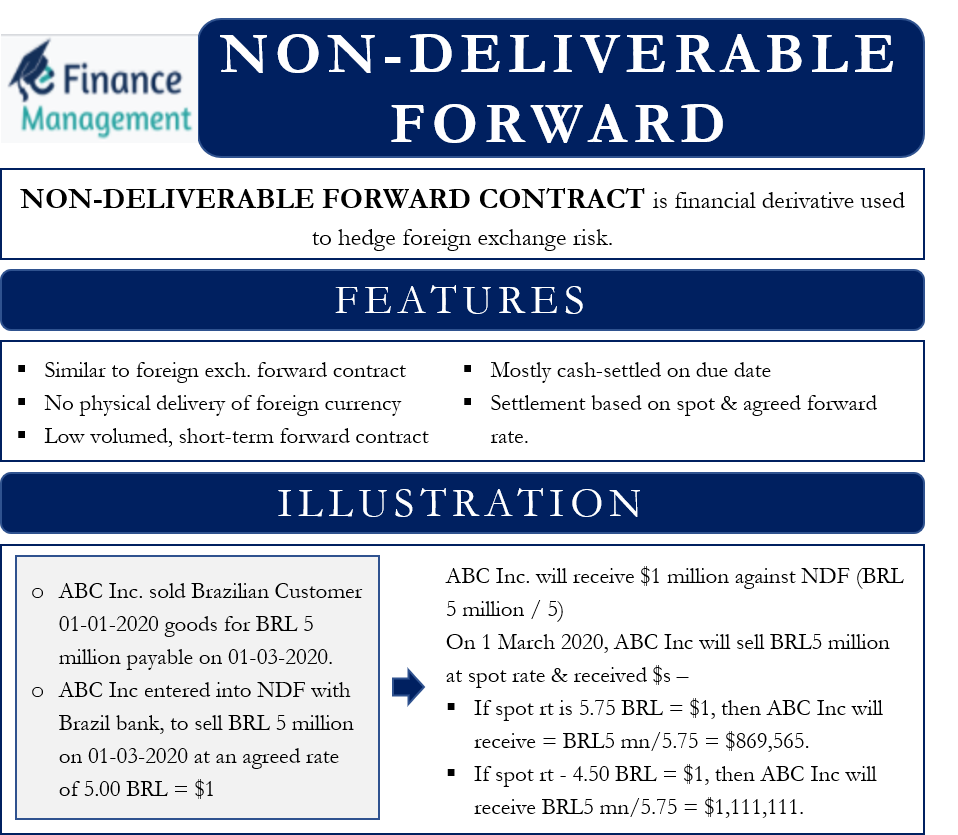

NDFs are very similar to foreign exchange forward contracts in the sense that it is a contract to buy or sell a specific quantity of foreign currency (non-convertible currency) at a pre-determined rate that will apply on a future date. However, unlike normal forward contracts, NDFs do not require the physical delivery of the underlying currency.

The NDF contract is cash-settled, mostly in US Dollars, on the due date (maturity). The settlement happens to depend upon the spot rate on maturity and the agreed forward rate. And the settlement will result in either a net receipt or a net payment between the parties to the contract.

So, the essence of such forward contracts is that it is for low volume, short-term forward contracts for non-convertible currencies and that get settled in cash only on the basis of the difference in the spot and forward price. These contracts take place for currencies as well as commodities. Therefore, no exchange of foreign currency or commodity takes place on the expiry. Instead, the difference only is settled in cash.

Why Non-convertible Currencies?

Some countries, especially emerging market economies, place restrictions on foreign exchange convertibility as they fear it might increase exchange rate volatility due to speculation caused by trading in forward markets.

Some of the currencies which actively participate in the NDF markets are the Korean won (KRW), Indian rupee (INR), Taiwan dollar (TWD), Chinese yuan (CNY), Indonesian rupiah (IDR), Malaysian ringgit (MYR), Philippine peso (PHP), Argentine peso (ARS), and the Brazilian Real (BRL).

How do Non-deliverable forward Contracts work?

The parties in any foreign exchange transaction always try to minimize or hedge the transaction risk, i.e., the risk that the exchange rate might change between the date of transaction and the final settlement date. NDFs are used to settle foreign exchange transactions between the parties involved. The bank is one of the parties to the transaction and is based in a country of non-deliverable currency. So, if the non-deliverable currency is Brazilian Real (BRL), the bank will be based in Brazil.

On the date of settlement, there is no exchange of foreign currency. The bank converts the foreign currency at the pre-agreed forward rate. However, depending on which way the spot rate has moved vis-à-vis the forward rate, the bank will either remit the difference between the spot rate and forward rate to the party or receive the difference from the party involved in the transaction.

Also Read: Forward Contract

Illustration

ABC Inc sold goods to its customers in Brazil on 1 January 2020 worth BRL 5 million. The Brazilian customer will pay ABC Inc. on 1 March 2020. ABC Inc is worried that by March 2020, the US dollar will appreciate against the Brazilian Real (BRL).

ABC Inc entered into a forward agreement (NDF) with Franco de Brasil, a Brazilian bank, to sell BRL 5 million on 1 March 2020 at an agreed rate of 5.00 BRL = $1

What will be the impact on the transaction when the spot rate on 1 March 2020 is

(a) 5.75 BRL = $1

(b) 4.50 BRL = $1

ABC Inc would have received BRL5 million/5 = $1 million guaranteed receipt against the NDF contract.

On 1 March 2020, ABC Inc will sell BRL5 million at the spot rate and received $s equivalent:

- In this case, the exchange rate went against ABC Inc, and so, as a result, they will receive less $.

At spot rate, ABC Inc will receive = BRL5 mn/5.75 = $869,565.

However, under the NDF, Franco de Brasil will pay ABC Inc the difference between spot and forward rate = $10,00,000 – $869,565 = $130,435

- In this case, the exchange rate went in favor of ABC Inc. Therefore, ABC Inc will receive more $.

At spot rate, ABC Inc will receive = BRL5 mn/5.75 = $1,111,111.

However, since the NDF was fixed at BRL5 million/5 = $1, ABC Inc will pay Franco de Brasil the difference between spot and forward rate = $1,111,111 – $10,00,000 = $111,111