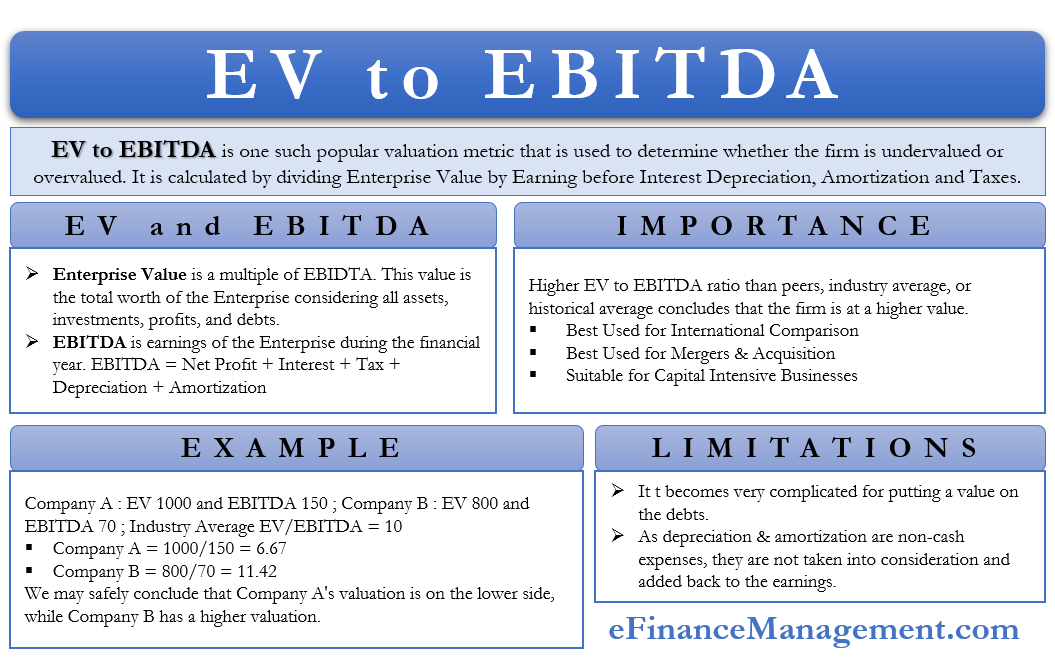

What is EV to EBITDA Multiple?

Enterprise Valuation ratios are used to determine the current value of the firm. And these ratios also help in determining whether the firm is undervalued or overvalued. EV to EBITDA is a popular valuation metric known as Enterprise multiple or EBITDA multiple. Therefore, through this metric, Enterprise Value calculation determines whether the firm is undervalued or overvalued. EV/EBITDA calculation happens by dividing Enterprise Value (EV) by Earnings before Interest Tax Depreciation & Amortization (EBITDA).

Enterprise multiple is a popular valuation metric that compares the firm (including its debt) to its EBITDA (substitute for free cash flow) for the financial year. This multiple becomes a reference point for all sorts of negotiations or understanding. What multiple of EBITDA is the right or reasonable value in case of a sale of Enterprise?

Formula

The formula for calculating this one of the important valuation metrics is below:

Enterprise Multiple = EV/EBITDA Or Enterprise Value (EV) / Earnings before Interest Tax Depreciation & Amortization (EBITDA)

Enterprise Value (EV)

EV, as we discussed above, is a multiple of EBIDTA. And this value represents the total value of the firm. In other words, this value is the total worth of the Enterprise considering all assets, investments, profits, and debts.

The analyst and negotiator use enterprise Value in the mergers & acquisitions deals to come up with a fair purchase price. Moreover, it is also used when an enterprise is hiving off or buying a division of a big enterprise. There are expert agencies who do this job of calculating the EV or the Firm Value.

Also Read: Enterprise Value

Market capitalization (Market price per share X No. of outstanding equity shares) is another metric used for the purpose. But that is not a fair representation of the enterprise value. Because it only considers the equity part of the firm and ignores the debt values. Thus, Enterprise Value considers the firm’s market capitalization as per the prevailing stock prices and cash & cash equivalents, preferred capital, and total debts and liabilities. Thus EV is an improved and modified version of market capitalization and is sometimes known as a “Takeover Price.”

In summary, Enterprise Value = Market capitalization+Prefered capital+a total of long term & short term debt – cash & cash equivalents-investments.

EBITDA (Earnings Before Interest, Tax, Depreciation & Amortization)

EBITDA is the earnings of the Enterprise during the financial year. It shows the quantum of net income, including non-cash expenses generated by the Enterprise during the financial year. And mostly, it acts as a substitute for the company’s cash flow. The calculation formula is:

EBITDA = Net Profit + Interest + Tax + Depreciation + Amortization

Or

EBITDA = Operating Income (EBIT) + Depreciation + Amortization

Let’s look at the Income statement to understand EBITDA better:-

| Particulars | Amount (Rs) |

| Net Sales | 500 |

| Less: Cost of Goods Sold (COGS) | 250 |

| Gross Profit | 250 |

| Less: Selling & Distribution expense | 50 |

| Less: Depreciation | 25 |

| Less: Amortisation | 15 |

| Operating Income (EBIT) | 160 |

| Less: Interest Expense | 20 |

| EBT | 140 |

| Less: Provision for taxes | 20 |

| Net Profit | 120 |

Now let’s calculate EBITDA using the above data:-

EBITDA using Net Profit = 120 + 20 (Interest) +20 (Taxes) + 25 (Depreciation) + 15 (Amortisation)= 200

OR

EBITDA using Operating Income (EBIT) = 160 +25 + 15= 200

Interpretation of EV to EBITDA

There is no standard thumb rule for interpretation of this multiple. Because it varies from business to business due to the sheer nature, the demand for the product, competition, profit margins, and capital requirements. Therefore, it isn’t easy to compare these multiple across industries. Of course, within the same industry segment, it may be comparable and throw light on the performance and valuation of the Enterprise. Nevertheless, a standard multiple of 10 or 10x is usually regarded as a fair value.

Undervalued or Overvalued?

A higher EV/EBITDA ratio than peers, industry average or historical average concludes that the firm is at a higher value. On the other hand, if this multiple is lower than peers, industry average, or historical average, then the firm is at a lower value. Therefore, the lower EV/EBITDA multiple comparatively makes the firm attractive for the investment. Because it looks undervalued, and benefits can continue to the buyer until the market realizes the same and valuation improves back to the industry average levels.

Also Read: Enterprise Value Calculator

However, the above interpretation stays correct only if the comparison is within the same industry and between the same peer groups. If not so, then this multiple stands incorrect. The general understanding is that sectors having high growth see a higher EV/EBITDA metric, and industries with low growth prospects see a lower metric. Therefore, only seeing a higher or lower valuation, one should not conclude that it is overvalued or undervalued.

Best Used for International Comparison

EV to EBITDA multiple helps compare two companies across countries because it avoids the impact of taxation policies on the earnings. The tax structure of one country differs from others, so this multiple completely overcomes taxation limitations and any such distortion in the valuation.

Best Used for Mergers & Acquisition

EV/EBITDA multiple is an ideal metric for valuation and is best used for mergers & acquisitions or splitting divisions to create separate entities or sales. Because market capitalization is not a right indication but misleading as it does not consider the effect of debts

Suitable for Capital Intensive Businesses

Enterprise multiple is best suitable for capital-intensive industries with hefty expenses on account of depreciation and amortization. And therefore, the operating earnings get subdued by these non-cash expenses.

EV to EBITDA or PE Ratio

Price-Earnings (PE) ratio or Market Capitalization Ratio ( Current Market Price / Earnings Per Share) is another most used. PE ratio tells us that the current market price or ruling market price of a company’s share is commanding how many multiples of its earnings per share. It also suggests what multiple or earnings, the market, and investors are ready to buy the shares of the company. Again, the P/E ratio conveys whether the ruling ratio is higher or lower than the market or industry segment. A lower ratio as compared to industry attracts buyers and vice versa.

However, though this ratio is also used for valuation, the EBITDA multiple is better than the PE ratio, as explained. Mainly this ratio fails to consider the debt part of the business and thus can’t represent the total or actual value of the Enterprise.

Irrespective of this, many investors prefer PE over Enterprise multiple as calculating the market value of debt sometimes becomes difficult. PE ratio is straightforward to compute.

Example of EV/EBITDA

Let’s understand Enterprise multiple with an example assuming both the companies operates in the same industry.

| Particulars | Company A | Company B |

| EV | 1000 | 800 |

| EBITDA | 150 | 70 |

Industry Average EV/EBITDA = 10

Company A = 1000/150 = 6.67

Company B = 800/70 = 11.42

Thus as shown in the above example, the Industry average is 10, while the multiple for Company A is 6.67 and that for Company B is 11.42. According to the above results, we may safely conclude that Company A’s valuation is on the lower side, while Company B has a higher valuation. As a result, Company A becomes an easy target for acquisition. Please note that this is only one of the tools to gauge, not the conclusion.

Limitations of EV to EBITDA

Here are a few limitations of this metric:

- While market capitalization calculation and thus, the measure of equity is easy. But it often becomes very complicated to put a value on the debts.

- As depreciation & amortization are non-cash expenses, they are not taken into consideration and added back to the earnings. However, ignoring them sometimes does not give the Enterprise a true and fair value. Particularly in a technology-oriented or fast obsolescence firm or where the machinery has a limited life.

Conclusion

Although the EV/EBITDA multiple does have its limitations, it is still the best multiple for valuation purposes. It is prevalent and provides for a reference point and understanding of whether the price put on the block is reasonable or not. It gives a fair idea to both parties during the Mergers & Acquisition process. Using Enterprise multiple along with other valuation multiples like PB ratio and PE ratio gives better results. Thus it is better to use this multiple with other complementary multiples for comparing across the same industry and scale instead of in isolation.