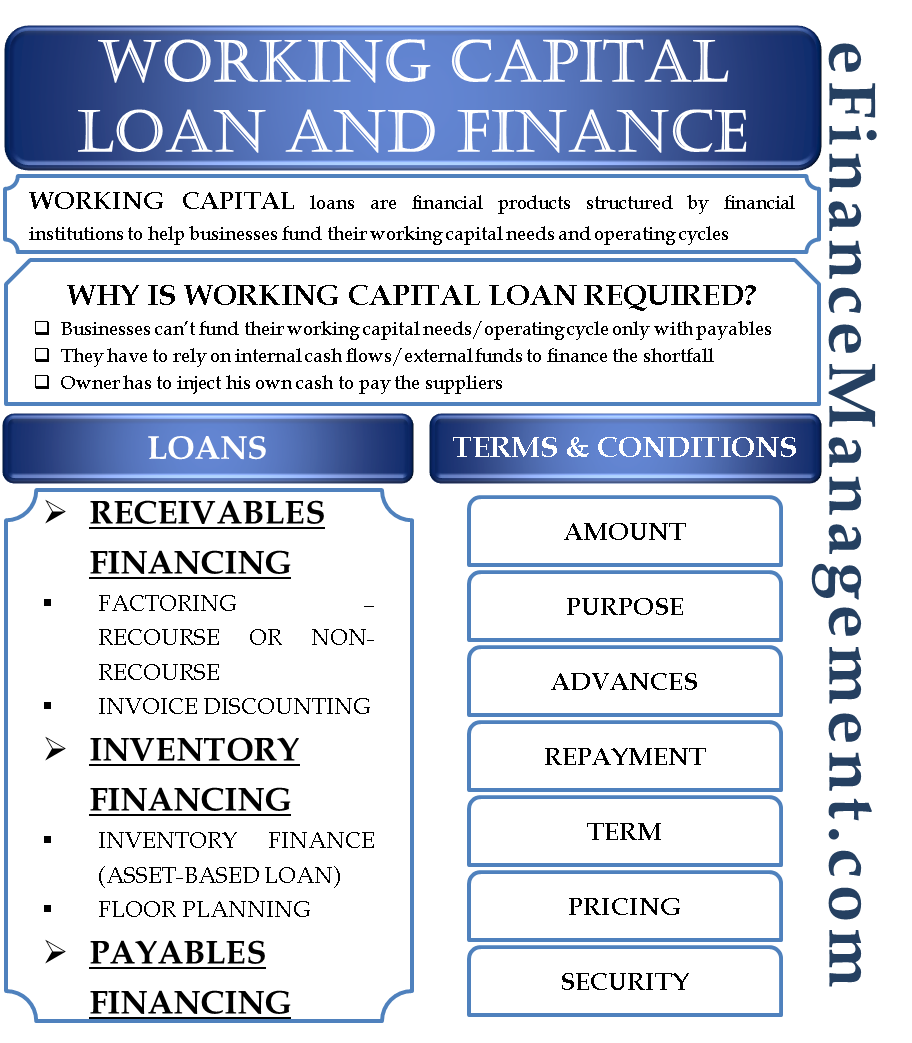

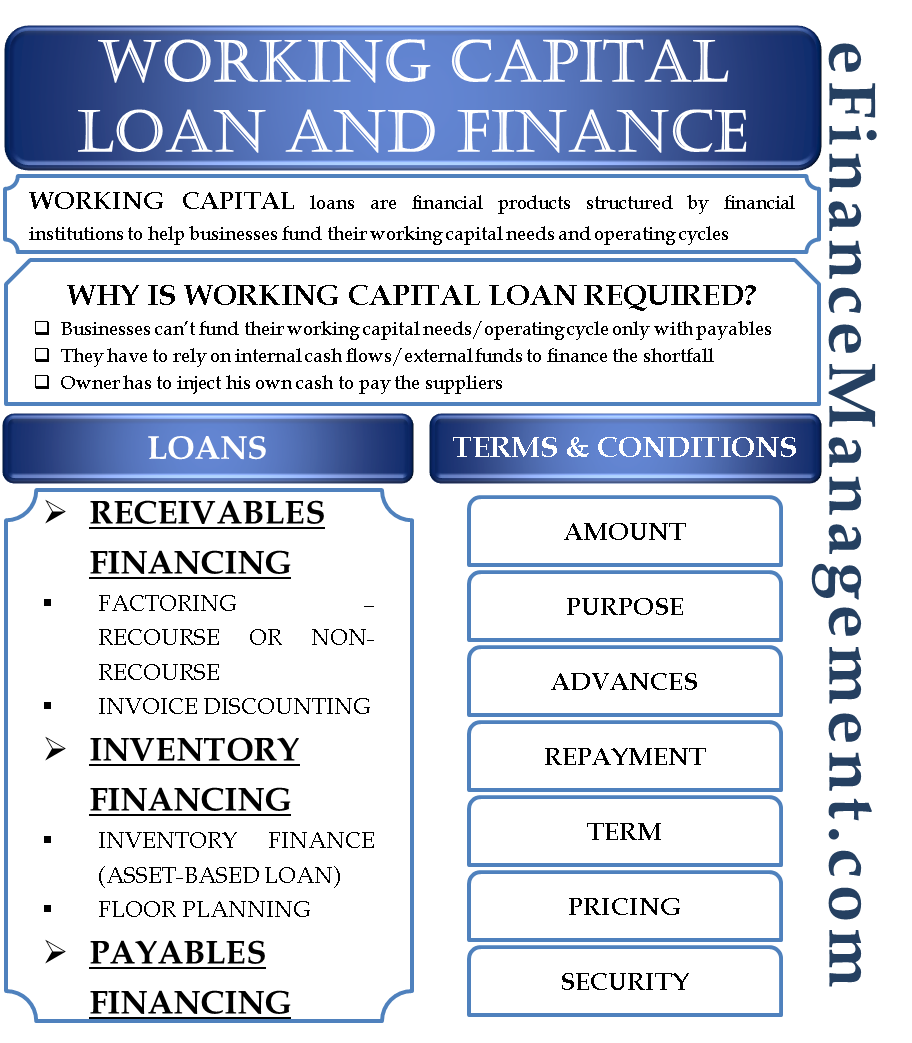

What is a Working Capital Loan?

Working capital loans are financial products structured by financial institutions to help businesses fund their working capital needs and operating cycles. The need for working capital arises due to the business cycle or, we can also say, the working capital cycle. A company’s working capital cycle is the total number of days it takes for a company to turn its inventory into cash. It is calculated as the number of days required to turn the inventory items into finished products and to collect the cash from the sale of these products.

The purpose of these loans limits to serve the short-term financing needs of a business. There are other financial products for long-term purposes like term loans, etc.

Why is Working Capital Loan Required?

The majority of businesses can’t fund their working capital needs or operating cycle only with payables. They have to rely on internally generated cash flows or external funds to finance the shortfall. It is also common in a small business that the owner will inject his own cash to pay the suppliers. Financial institutions have come up with different products, working capital loans, to solve this problem and help businesses generate additional liquidity to finance their working capital gap.

Working Capital Loans

Working capital loans range from a plain vanilla short-term loan to a highly structured facility to securitize receivables. They provide additional liquidity to a company by either monetizing short-term assets, such as account receivables and inventory, or postponing cash outflows related to account payables.

Working capital loans arrangement is usually by a third-party financial institution that will act as an intermediary between a company and its suppliers or clients. The most common loan structures are as below in the table.

Receivables Financing |

Factoring–recourse or Non-recourse |

Factoring is the sale of account receivables to a third-party, often a financial institution, at a discount, usually ranging from 2% to 8%. The facility can be structured as an off-balance sheet if it is a true sale with limited recourse to the seller. |

Invoice Discounting |

Invoice discounting is a loan by a financial institution with the account receivables as collateral. The quality and liquidity of the receivables will determine the exact amount and pricing of the facility. | |

Inventory Financing |

Inventory Finance (Asset-based Loan) |

This is an asset-based loan secured by the inventory or a part of the inventory, such as work-in-progress or finished products. The amount will be determined by the realizable value of the inventory and pricing will be determined by the creditworthiness of the borrower and the quality of the inventory. |

Floor Planning |

A lender will purchase the inventory, and, as the inventory is sold, the company will repay the debt. This method of financing is often used by a company with a strong balance sheet, such as car dealers. | |

Payables Financing |

Payables Funding |

The bank will pay the supplier promptly in cash when he will issue the invoice and the company will repay the bank at a later date. The company will effectively stretch its payables and benefit from better payment terms. Payables facilities are usually provided on an unsecured basis, but a bank could require a guarantee depending on the creditworthiness of the counterparty. |

For an overview of the various sources of working capital finance, please refer to our post – Working Capital Financing.

General Terms & Conditions of a Working Capital Loan

The specific terms and conditions relating to working capital loans are set forth in credit agreements that the lawyers prepare. The main provisions of these contracts are as below.

Amount

The amount of the credit will depend on the creditworthiness of the counterparty, the value of assets they can pledge, inventory levels, or outstanding receivables.

Purpose

Companies get these loans for general corporate purposes. This includes the purchase of raw materials, the payment of wages and bills, etc.

Advances

Advances for these loans are typically provided on a short-term basis and in line with the payment terms, typically 30-day, 60-day, and 90-day.

Repayment

Working capital loans can be provided on a revolving basis so that the company can borrow and repay loan advances with flexibility. The bank can also design flexible repayment terms that will follow cash flow patterns, which is useful for seasonal businesses. Bullet repayments are less common for working capital loans.

Also Read: Sources of Working Capital

Term

Working capital loans are provided on a committed basis. Usually up to five years or an uncommitted basis.

Pricing

Pricing is usually based on a reference floating rate such as LIBOR, to which a spread reflecting the credit risk of the borrower is added. A working capital loan pricing is usually lower than other credit facilities. This is because of the short-term nature of the instruments and the collateral provided by the inventory or receivables.

Security

For more risky borrowers, the lender may request collateral on the company’s assets, including the receivables and inventory.

Great article! This article will definitely help me to get instant cash for my working capital. This definitely helps me to be more knowledgeable about working capital loan. Thanks for sharing this article.

Want to discuss about loan against LC for overseas project..please contact +91 9818987755.