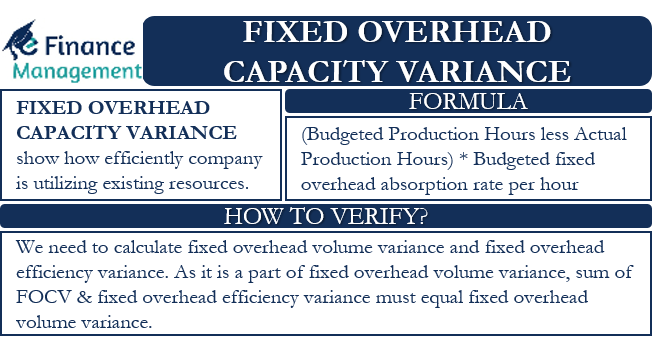

Fixed Overhead Capacity Variance (FOCV) basically shows how efficiently a company is utilizing its existing resources. In simple words, we can say that it compares the utilization of budgeted and absorbed resources. Usually, the more the absorbed resources, the better it is. This is because it means there was less or no idle capacity, or the workers didn’t sit idle. Note that the actual number of hours in the Fixed Overhead Capacity Variance can never be more than the budgeted hours.

So, we can say that the FOCV is the difference between the fixed overheads attributable to the change in the number of manufacturing hours and the budgeted fixed overheads.

FOCV tells about the under or overutilization of the absorbed fixed overheads because of the variance between the budgeted labor working hours and the actual number of hours worked. It basically represents the number of hours that the laborers could have used, but they did not, or they worked for more hours. Such a situation may arise because of a labor strike, failure of machinery, overtime work, and more.

Relation with Fixed Overhead Volume Variance

FOCV is one of the two parts of the Fixed Overhead Volume Variance. The other one being Fixed Overhead Efficiency Variance.

The Fixed Overhead Volume Variance is the difference between the budgeted fixed overhead costs on the basis of production volume and the actual fixed overhead costs.

Following is the formula to calculate Fixed Overhead Volume Variance (FOVV):

FOVV = (Standard Hours allowed for actual production volume * Fixed Overhead absorption Rate) Less Budgeted Fixed Overheads

OR Budgeted Fixed Overhead Less Fixed Overhead Applied/Absorbed

Similarly, Fixed Overhead Efficiency Variance (FOEV) is the difference between the absorbed fixed production overheads attributable to any change in the production efficiency. It is on the basis of change in the manufacturing hours.

Following is the formula to calculate Fixed Overhead Efficiency Variance:

FOEV = (Standard Production Hours less Actual Production Hours) * FOAR

Here FOAR is the Fixed Overhead Absorption Rate/unit of hour

Formula and Example of Fixed Overhead Capacity Variance

Following is the formula to calculate the Fixed Overhead Capacity Variance:

FOCV = (Budgeted Production Hours less Actual Production Hours) * Budgeted fixed overhead absorption rate per hour

Similar to other variances, Fixed Overhead Capacity Variance can also be favorable or adverse (unfavorable). FOCV will be favorable if there is over-absorption of fixed overheads because of more hours worked than the budgeted. The FOCV will be unfavorable or adverse if the fixed Overheads are under-absorption. This could be because of inefficient labor.

Let us take a simple example to better understand the calculation of the FOCV:

Company A has actual production of 275,000 units and budgeted production of 250,000 units. The standard fixed overhead absorption rate for Company A is $2,000 per unit. It has standard machine hours per unit of 10 hours, and the actual number of machine hours is 3,000,000.

To calculate the FOCV, we first need to find the budgeted production hours. This will be 2,500,000 (250,000 x 10).

Now, we need to subtract the budgeted production hours from the actual production hours. Or, 2,500,000 less 3,000,000 = 500,000

Now, we need to multiply it with the Fixed Overhead Absorption Rate per unit of an hour (Fixed Overhead Absorption Rate/unit of an hour.

Also Read: Fixed Overhead Volume Variance

FOCV = 500,000 * (2000/ 10) = 100,000,000

This variance is favorable because Company A was able to work for more manufacturing hours than the budgeted.

How to Verify Fixed Overhead Capacity Variance?

We can cross-verify this answer as well. But for that, we need to calculate the Fixed Overhead Volume Variance and Fixed Overhead Efficiency Variance. Since FOCV is a part of Fixed Overhead Volume Variance, the sum of FOCV and Fixed Overhead Efficiency Variance must equal Fixed Overhead Volume Variance.

To calculate Fixed Overhead Efficiency Variance, we first need the Standard production hours. This will be 275,000 * 10 or 2,750,000. Now, we need to subtract the Actual production hours from the Standard production hours.

So 2,750,000 less 3,000,000 = 250,000. Now, we need to multiply it by the Absorption Rate per unit hour (from above)

Fixed Overhead Efficiency Variance = 250,000 * 200 = 50,000,000

This variance is unfavorable because of the use of more manufacturing hours for producing 275,000 units than the standard hours.

Now, we need to calculate the Fixed Overhead Volume Variance. For this, we need to subtract the Absorbed Fixed Overheads from Budgeted Fixed Overheads.

= (275,000 x $2,000) less (250,000 x $2,000) = $5000,0000. This variance is favorable

To cross verify the answer, we need to add Fixed Overhead Capacity Variance and Fixed Overhead Efficiency Variance.

= $100,000,000 (F) plus $50,000,000 (U)

Fixed Overhead Volume Variance = $50,000,000 (F)

Since we got the same answer for Fixed Overhead Volume Variance from both calculations, our answer is correct.

Final Words

Fixed Overhead Capacity Variance gives relevant information on the idle capacity or about the utilization of resources. Management can use this information for better resource planning and budgeting. For cost optimization and optimum utilization of the resources, it is very crucial to reduce or eliminate idle time or idle resources. This is because it means the company is spending on resources that are not contributing anything.

RELATED POSTS

- Fixed Overhead Spending Variance – Meaning, Formula, Example, and More

- Fixed Overhead Calendar Variance – Meaning, Formula, and Examples

- Variable Overhead Efficiency Variance – Meaning, Formula, and Example

- Variable Overhead Cost Variance – Meaning, Formula, and Example

- Production Volume Variance: Meaning, Formula, Limitations, and More

- Variance Analysis Formula with Example