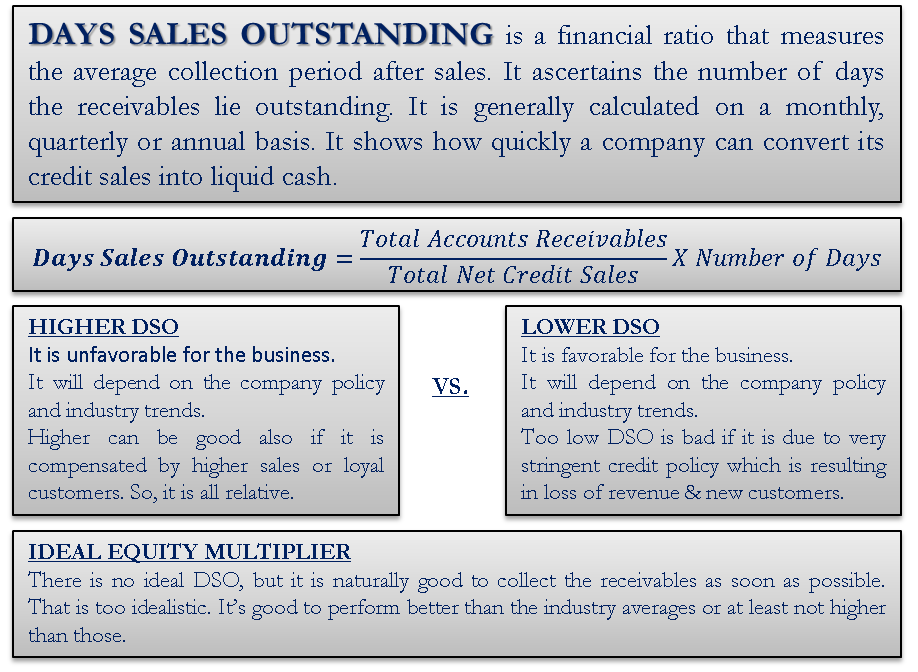

What is Days Sales Outstanding (DSO)?

Days sales outstanding is a financial ratio that helps calculate the number of days the accounts receivables remain outstanding. It is a way to measure the time taken by a company to convert its credit sales into cash. This financial ratio reveals the management of accounts receivables of the company. DSO can be calculated monthly, quarterly, or annually over various time periods.

Formula and Calculation with Example

DSO can be calculated by dividing the total accounts receivables by total net credit sales during a particular period of time. The resultant should be multiplied by the number of days in the period of time. Most commonly, it is calculated annually and multiplied by 365 days in the end.

A lower days sales outstanding ratio shows that the company can collect its receivables in lesser time. However, a higher days sales outstanding ratio indicates that a company takes a longer time to collect its accounts receivables.

It should be noted that if the DSO resultant is very close to the payment day given to the customer, the company’s credit policy is too stringent.

Also Read: Days Inventory Outstanding

Formula

The formula for calculating DSO is:

Days Sales Outstanding = Total Accounts Receivables / Total Net Credit Sales x Number of Days

Days Sales Outstanding Calculation (Example)

Calculation using Example

Let us understand the calculation of DSO through the following example.

Carl & Dan International Limited shows a sales revenue of $350000 for the month of January 2015. Their cash sales amount to $150000 while their net credit sales amount to $200000 (remaining amount of sales). Their month-end financial statements of Carl & Dan International Limited show that their accounts receivable stand at $100000. The Company generally wants to collect the accounts receivables within 20 days from its customers.

Using the Days sales outstanding formula given above,

Days sales outstanding = Total Accounts Receivables / Total Net Credit Sales x Number of Days

= $100000 / $200000 x 30

= 15 days

Thus, the DSO figure for Carl & Dan International Limited is 15 days. This implies that the company takes around 15 days to collect its accounts receivables. This is a good ratio for Carl & Dan International Limited as it aims at collecting its accounts receivables within 20 days.

Analysis

For any business, it is always suitable to have liquid funds. Therefore, easy and quick conversion of net credit sales into cash is preferable.

Lower DSO

- When days sales outstanding figure shows a lower value, it is favorable for the business.

- It will depend on the company policy and industry trends.

- Too low DSO is bad if it is due to a very stringent credit policy resulting in loss of revenue & new customers.

Higher DSO

- While a higher figure of days outstanding sales indicates an unfavorable position of the business.

- It will depend on the company policy and industry trends.

- Higher is good also if higher sales or loyal customers compensate it. So, it is all relative.

Ideal DSO

There is no ideal DSO, but it is naturally good to collect the receivables as soon as possible. That is too idealistic. It’s good to perform better than the industry averages.

It is advisable to maintain a monthly or annual trend of days sales outstanding. It helps the business to assess any significant increase or decrease in the ratio. This ensures that the management of the company’s accounts receivables is efficient.

You can also refer to Debtors / Receivable Turnover Ratio and Collection Period.

Importance of Calculation of DSO for a Business

From a business point of view, it is better to collect accounts receivables as quickly as possible. DSO is an important tool for assessing the liquidity of the business concern. The more liquid the business’s current assets, the more flexible its operations are. Therefore, the calculation of DSO is an important accounting tool for any business.

Conclusion

Days sales outstanding ratio is an important accounting tool for a business, but it should not be considered the only tool for maintaining liquidity. Sometimes figures revealed by days’ sales outstanding do not indicate the actual efficiency of the business. This is because the sales volume affects the calculation of days sales outstanding. For instance, an increase in sales can also show a low days sales outstanding figure.