Option pricing models are financial models used for the purpose of valuing options. The premium paid for buying an option is the value of that option. Now, you might have a question “When the premium of an option is already quoted in the market, what is the need to calculate option valuation?”. The option valuation tells whether the option is underpriced or overpriced or whether it is fairly priced. Therefore, it helps in arriving at the conclusion of whether you should buy an option or sell it. This article attempts to explain the most prevalent and widely acknowledged option pricing models. But before getting into the depths of an option pricing model, it is important to first understand what are the components of option premium.

Components of Option Premium

An option is the sum of its intrinsic value and its time value.

| Option Premium = Intrinsic Value of Option + Time Value of Option |

Intrinsic Value of Option

The intrinsic value of an option is the difference between the strike price and the market price of the security if such an option is in the money (in simple terms if it becomes exercisable).

A call option turns in the money if the market price is more than the strike price. The formula to calculate the intrinsic value of a call option is:

| Intrinsic Value of Call Option = Market Price of Security – Strike Price |

A put option turns in the money if the market price is less than the strike price. The formula to calculate the intrinsic value of a put option is:

| Intrinsic Value of Put Option = Strike Price – Market Price of Security |

Time Value of Option

The time value of an option is basically the balancing figure derived by subtracting its intrinsic value from the premium amount.

| Time Value of Option = Option Premium – Intrinsic Value of Option |

The time value of an option is the portion of its premium that reflects the uncertainty of the option’s future price movements, given the remaining time until expiration. It is the value that traders are willing to pay above the intrinsic value of the option. There are several factors that affect the time value of an option. These include the volatility of the underlying asset, the time remaining until expiration, and the level of interest rates. Therefore, one should be well-versed with the factors affecting option pricing.

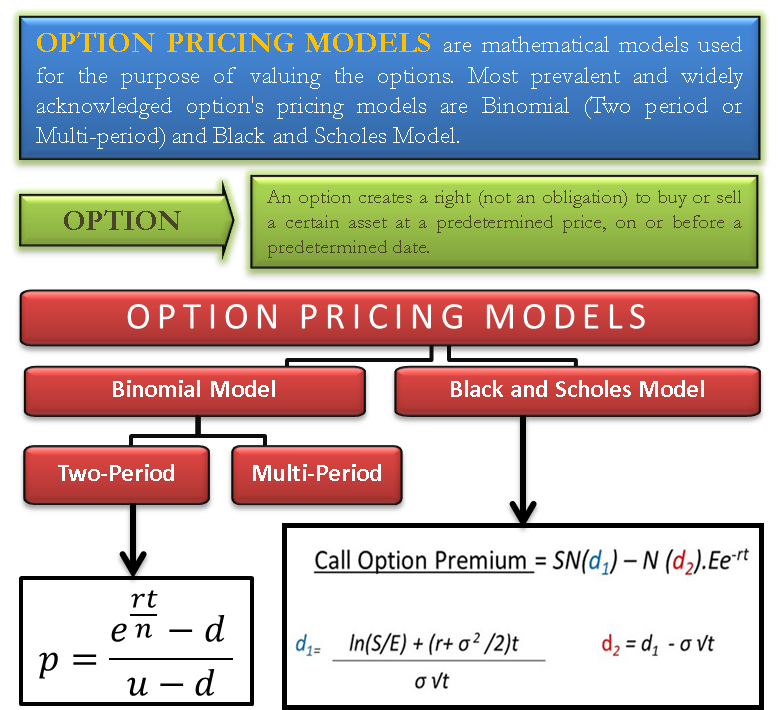

Option Pricing Models

There are two approaches to option pricing models: the traditional approach and the modern approach.

The following three option pricing models follow the traditional approach:

- Binomial model

- Portfolio replication model

- Risk neutral model

And, the Black & Scholes model follows the modern approach.

A point to note is that all the models under both approaches tend to find the value of the call option. In order to calculate the value of the put option, one should find the value of the call option with the same strike price as the put option. Then the put-call parity theory formula uses this value of the call option to derive the value of the put option. Let’s begin learning about the option pricing models.

Risk Neutral Model

The risk-neutral option pricing model is a mathematical framework for valuing options. It is based on the assumption that traders are indifferent to the risk and make investment decisions based solely on expected returns. The key assumption of the risk-neutral option pricing model is that the expected return on the underlying asset is equal to the risk-free rate of return. Therefore, the probability of each possible price movement of the underlying asset is calculated in such a way that the expected rate of return on the asset is equal to the risk-free rate of return. This allows traders to calculate the fair price of an option by discounting its expected future payoff at the risk-free rate of return.

Binomial Option Pricing Model

The binomial option pricing model assumes that there exist only two possible prices for the forthcoming period. And, the two prices are the ones realized on an uptick or downtick. According to this model, the price of an option is equal to the difference between the present value of the stock (as computed through a binomial tree) and the spot price.

Portfolio Replication Model

The basic idea behind this model is that if a portfolio of underlying assets can be constructed that has the same payoff as the option, then the value of the option must be equal to the value of that portfolio. To construct the replicating portfolio, traders need to determine the appropriate weights of the underlying assets in the portfolio. This is done by solving a system of equations based on the option’s payoff function and the prices of the underlying assets.

Black and Scholes Option Pricing Model

This model is particularly used to value European options held to maturity. This formula was derived by Fischer Black and Myron Scholes, who went on to win the Nobel Prize for this discovery. Before discovering this formula, options trading was considered a gamble that has no mathematical or scientific basis. It was this formula that explained the rationale behind options trading. Immediately following the release of this formula, the market noticed a dramatic surge in the volume of options trading. Though dated, present-day analysts and brokers borrow heavily from the B&S option pricing model. This is a testimony to the accuracy and precision behind the formula.

The formula of Black & Scholes model is:

Monte-Carlo Simulation Method of Option Pricing

Monte Carlo simulation is a method for valuing options by modeling the evolution of the underlying asset price over time and simulating a large number of possible price paths. It is based on the assumption that the underlying asset price follows a stochastic process that describes the random fluctuations of the asset price over time.

Monte Carlo simulation is particularly useful for valuing complex options with non-linear payoffs, such as barrier options or American options. By simulating a large number of possible price paths, traders can accurately value these options and make informed investment decisions.