What is a Proxy Fight?

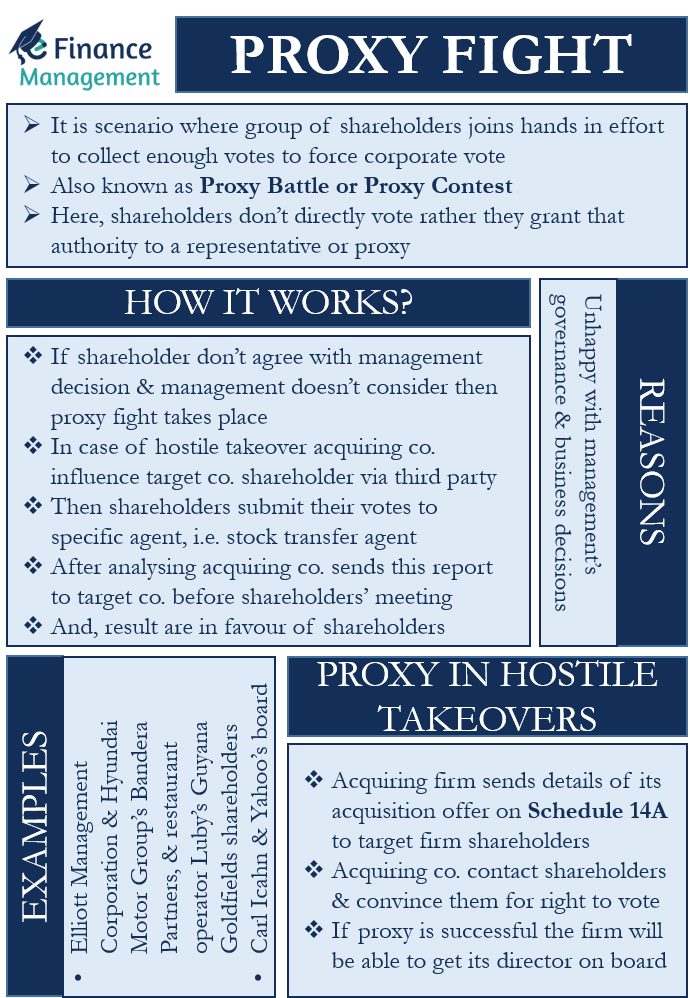

A proxy fight is a scenario where a group of shareholders joins hands to collect enough votes to force a corporate vote. The primary motive of a proxy battle is to gather enough shareholder votes, enough voting power, and support to get the results they want. Other names for such an action are proxy battle or proxy contest.

Shareholders generally come together to oppose any management decision or vote out the existing management at the annual general meeting (AGM). Also, we see such a scenario in the case of corporate takeovers. For instance, in case of a hostile takeover, the acquirer may convince the existing shareholders to vote out some or all of the firm’s senior executives who are opposing the takeover. This would make it easy for the hostile bidder to take control of the company.

Generally, shareholders do not directly vote at a company’s meeting. Instead, they grant that authority to a representative or proxy. And this representative or proxy will vote on behalf of the shareholders. This is the reason why we call it a ‘proxy fight’ and not a ‘shareholders’ fight.’

Proxy Fight: Reasons and Real-World Examples

After a firm goes public, the management starts working as the employee of the shareholders. Therefore, it becomes necessary for the management to understand that they can no more run the business as per their wishes. Or unlike owners, as they used to be working before going public. And this throws a responsibility on them to work in the interest and for the benefit of the shareholders. But, when the management gives less priority to shareholders’ interests, it leads to unrest and possibly a proxy fight.

Generally, common shareholders get the right to vote on the following management actions:

- Making any changes to the corporate governance documents.

- Any merger or acquisition.

- Dissolution of the firm.

- Selling a significant portion of the company’s assets.

- Electing directors.

Though there are many reasons for initiating a proxy battle, in the real world, the main reason why major shareholders go for a proxy battle is when they are unhappy with the management’s governance and business decisions.

Real-World Examples

Let us discuss a few such most popular examples of the real world where proxy fights took place.

Elliott Management Corporation, a U.S. hedge fund, was not happy with Hyundai Motor Group’s dividend and corporate restructuring plan. Elliott thought that Hyundai’s decision lacked rationale and would hurt the shareholders.

Bandera Partners, an activist investor, was not happy with restaurant operator Luby’s management decisions. The activist investor wanted the company to change its debt structure and work to turn around the declining same-store revenues and traffic.

Guyana Goldfield’s shareholders weren’t happy with how the management ran the business. The company was facing rising pressure from the shareholders to turn around its performance. And after a long flight, the CEO lost his job, and the company had to appoint two independent directors.

Also Read: Hostile Takeover

In May 2008, billionaire Carl Icahn made an effort to replace Yahoo’s board using a proxy fight.

How does it Work?

First, the shareholders who do not agree with the management’s decision need to make management aware of their issues. Now, if the management refuses or does not agree with the views of those shareholders, then those shareholders may try to gather proxy votes to force the change they want.

Such shareholders will try to convince other shareholders to use their votes to force the change. The change could be to force any decision, oppose any decision, replace any board member, etc.

In case of a corporate takeover, the acquiring and the target firm could use several solicitation methods to swing the shareholder votes. It is also possible that the firm sends Form DEF 14A (or a proxy statement) to shareholders. This form carries all the details on the target and acquiring company.

Usually, the acquiring company tries to influence the target company shareholders via a third party. This third party, usually a proxy solicitor, may contact each shareholder individually to explain the plans of the acquiring company.

Now, the shareholders need to submit their votes to a specific agent, who is usually a stock transfer agent. The proxy solicitor may then analyze all the votes to identify unclear votes or the shareholders who voted more than once, or those who did not vote at all.

Then the acquiring firm sends all these analyses to the target firm’s board before the shareholders’ meeting. Finally, the management decides based on shareholders’ votes.

Is Proxy Fight Successful?

It is normally seen that some shareholders do not show much interest in the company’s day-to-day operations or its management decisions. These shareholders are relatively easier to sway. This is because such shareholders generally go with the recommendations they get without examining the merits behind them.

Such behavior helps the acquiring company if the financial results of the target company are not good or are hurting the shareholders. In such a case, the acquiring company can easily win shareholder votes by pitching ideas that would benefit the shareholders.

Another strategy that can help in a proxy battle is to get support from mutual funds and hedge funds. This is because mutual and hedge funds hold a large number of shares, and thus, they could gather a large number of proxy votes.

Despite such strategies, proxy fights are generally difficult to win, and most of such battles are unsuccessful. This is because companies put in place many corporate governance tactics that make it hard for the shareholders to win these battles. The tactics that companies use are:

Staggered Board – such a clause prevents shareholders from replacing the entire board in one go. For instance, there could be a clause that only 20% of the board can be replaced in a year.

Golden Parachute – it is mainly a defensive strategy. This strategy implies that directors should be paid a big amount of money if they are asked to leave in case of a takeover.

Proxy Contests in Hostile Takeovers

In case of a hostile takeover, the acquiring firm sends details of its acquisition offer on Schedule 14A to the target firm shareholders. Generally, the acquiring firm uses the services of the proxy advisory firm. This firm is responsible for preparing the shareholders list, contacting them, as well as explaining the offer of the acquiring firm to the shareholders.

Further, the acquiring firm requests the shareholders to grant them the right to vote as a proxy. Now, if the proxy battle is successful, the acquiring firm would be able to get its directors on the board. These directors will then approve the acquisition offer from the acquiring firm.

Final Words

A proxy fight is an effective weapon that allows shareholders to fight for what they believe is right. It is always desirable that shareholders do not use this weapon. But, if a need arises and they are not happy with the management decisions, then they should not shy from using this strategy.