Meaning

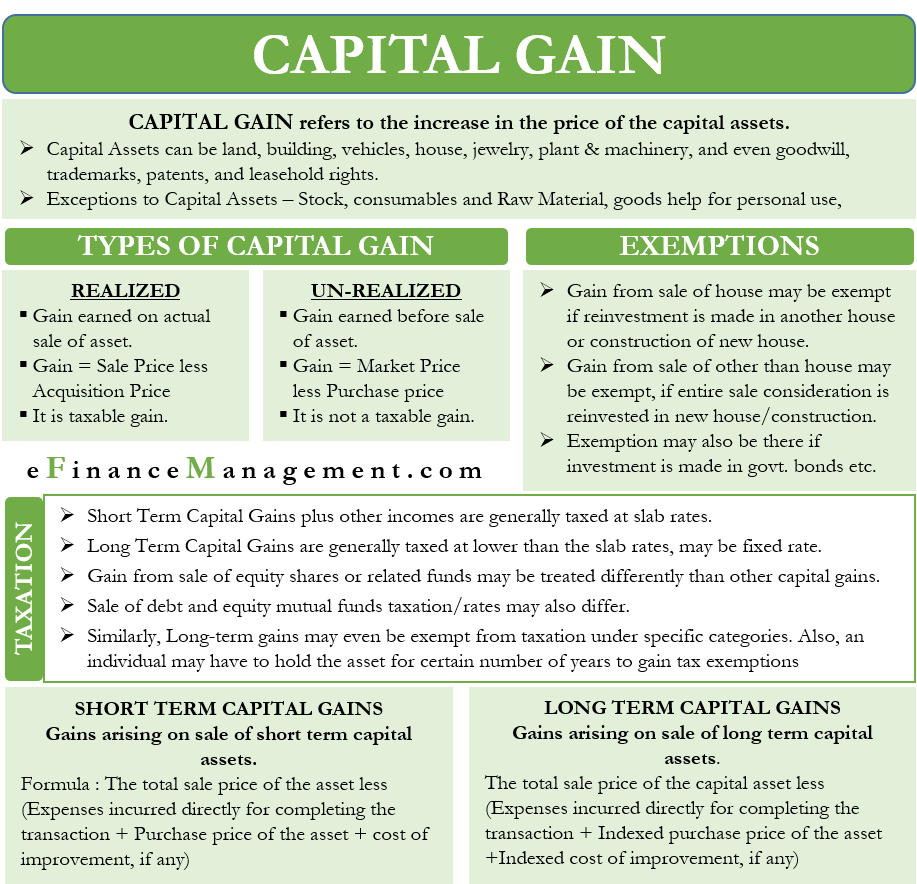

Capital gains are an increase or rise in the price of a capital asset from its purchase price. Capital assets can be land, building, vehicles, house, jewelry, plant and machinery, and even goodwill, trademarks, patents, and leasehold rights.

There are a few exceptions to the category of a capital asset. Stock, consumables, or raw materials are not capital assets for business or trade purposes. Similarly, the exclusion from this category is there for items or goods held for personal use like furniture or a garment. Few countries do not include agricultural land and even gold or a particular class of bonds under the ambit of a capital asset.

A capital loss is the opposite of a capital gain. It is the decrease or fall in the price of a capital asset from its purchase price.

Types of Capital Gains

Capital gains are of two types- “realized” or “unrealized.” A Realized capital gain is one when the sale of the capital asset is over, and an increase or profit out of the deal is earned. Such increases are taxable.

Also Read: Dividend vs Capital Gains

On the other hand, “unrealized” capital gain is the gain or profit where the asset sale transaction is pending, so no benefit has taken place. The prevailing price of the capital asset under consideration is higher than its acquisition or purchase price. But the final sale is not yet complete. Such gains are not taxable. But still, they have to be mentioned for accounting purposes sometimes.

The “realized” category of capital gains has two classifications, “short-term” and “long-term” gains. A seller may sell a capital asset for the period of one year and earn profits. Such gains are “short-term capital gains.” Where a seller sells a capital asset after holding it for over a year, such gains are “long-term capital gains.”

An individual can get a capital asset as a gift or from a will, succession, or inheritance. In such a scenario, the time calculation also includes the holding period with the previous owner of that asset. The total period thus calculated will be taken into account to decide if the gain is short-term or long-term.

Taxation of Capital Gains

The gain plus the income of the taxpayer is the basis for taxation in case of short-term capital gains. Tax calculation, according to the rate of taxation of his slab of income, will be done.

Long-term capital gains are generally taxable at a rate lower than the income-tax slab rate of the taxpayer. For example, suppose a person is in the tax slab of 30%. Then too, he may have to pay only a 15% tax on his gains. But in some countries, such gains are taxable at a fixed rate, irrespective of the individual’s tax-slab rate. Also, the gains from the sale of equity shares or related funds may be treated differently from the gains from other capital assets.

Taxation of capital gains from the sale of debt and equity mutual funds may also differ. The taxation rates may differ for a specified category of mutual funds, even in debt and equity mutual funds. Similarly, Long-term gains may even be exempt from taxation under specific categories. Also, in some cases, an individual may have to hold the mutual fund for a particular number of months/ year. The period is often more than 12 months. Then his gain will come under long-term capital gains exemptions.

Calculation

Capital gains are taxable in the year of sale or transaction. It is irrespective of the fact that the sale amount has changed hands or not. Also, any cost of the improvement will be under consideration for calculating these gains. The cost of improvements includes expenditure incurred of a capital nature to make a permanent improvement or addition to the capital asset under consideration. A seller may acquire a capital asset by means other than an outright purchase. In such cases, the cost of the improvement by the previous owner is also undergoing indexation.

Short-term Capital Gains

The formula for short-term gains calculation is:

The total sale price of the asset less (Expenses incurred directly for completing the transaction + Purchase price of the asset + cost of improvement, if any)

Long-term Capital Gains

Long-term capital gains can relate to the sale of a capital asset purchased many years ago. Taking its historical purchase price for calculation is unfair and will result in an inflated gains figure. Therefore, if any, indexation of the cost of acquisition or improvement is done by applying the cost inflation index or CII.

The calculation of the indexed cost of acquisition is the as- Purchase price, or cost of procurement of the capital asset x cost inflation index for the current transfer or sale year/ cost inflation index for the year of purchase. The indexation of the cost of improvement also happens similarly.

Now, we can calculate long-term capital gains as:

The total sale price of the capital asset less (Expenses incurred directly for completing the transaction + Indexed purchase price of the asset +Indexed cost of improvement, if any)

Exemptions

There are few exemptions for the taxation of capital gains under specific conditions. These conditions are as per the Income Tax act of the respective countries. Gains from the sale of a house may be exempt from taxation. It is so where reinvestment happens into buying or constructing another house property. Similarly, gains from an asset other than a house can also be exempt from taxation. It is so where the investment of the entire sale consideration and not just the gain in buying or constructing a new house property happens. Also, it provides for exemptions on taxation of capital gains if the investment of the gain happens into specific government bonds. Various exemptions are available on the sale or transfer of agricultural land as well.

The above examples of exemptions may vary from country to country. Also, various conditions have to be met too. These are in accordance with the respective Income Tax Acts of those countries.