Understanding the concept of direct and indirect cost is very important from the viewpoint of assignment of various costs to products (the cost objects). The most important term for understanding and correct classification of the costs into direct and indirect is traceability. Cost traceability is nothing but a clear cause and effect relationship between the incurred costs and the cost object. Let us look at a detailed explanation with an example.

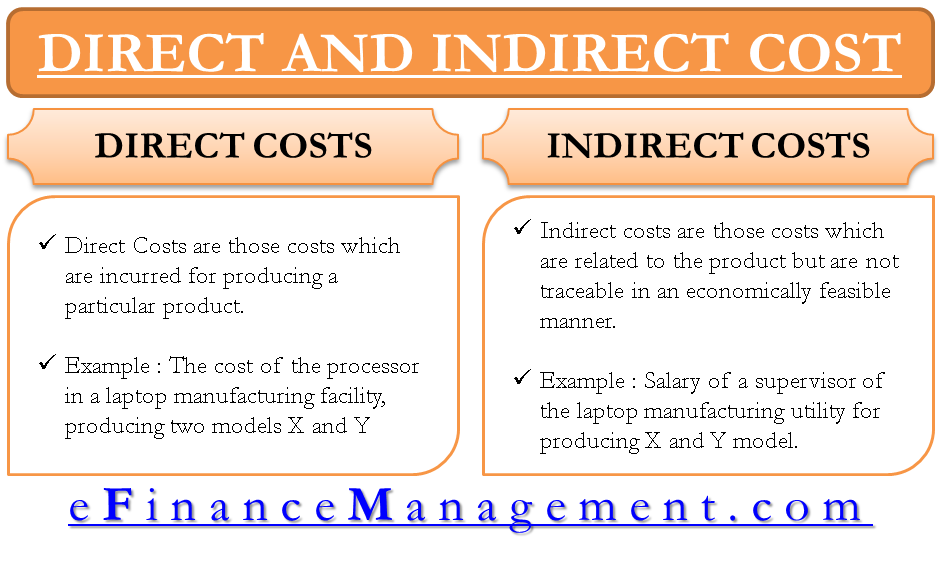

Direct Costs

Indirect Costs

Indirect costs are related to the product but are not traceable in an economically feasible manner.

Example: Salary of a supervisor of the laptop manufacturing utility for producing X and Y models. Why? It is simple. The supervisor supervises X model of laptop and Y too. But, it isn’t very easy to say how much cost should be assigned to X and Y., And finding out that may not be economically feasible. Here, we can see the relatedness is there since the manufacturing of X laptop requires the supervision of the supervisor. Still, the traceability is not there as it is very difficult to trace how much supervision is on which model of laptop. The cause and effect relation between the product, say Model X, and the supervision cost is not direct and clear.

| Direct Costs | Indirect Costs | ||||

| Direct Material | Direct Labor | Direct Expenses | Indirect Material | Indirect Labor | Indirect Expenses |

Direct costs are assigned to product-based the relationship between the costs and the cost object, whereas indirect costs are allocated based on some logical base.

To find the exact costing of a product, it is always desirable to have most of the costs as direct costs. But such a scenario is not practically possible. There are two main factors that affect the classification of costs into direct and indirect.

Materiality

If a particular cost is enormous in value, the cost incurred for tracing that cost may be affordable by the management. Another reason for the higher amount of effort put in for tracing the cost is that the impact on the final product cost would be huge if this high cost is assigned to products wrongly. So smaller the amount of cost, the lower is its traceability.

Information Gathering Technology

The technology employed for tracing the costs is also very important because it becomes easy to trace costs with the help of improved technology. The big organization focuses a lot on information and reporting systems. Therefore, they can outline even the smaller costs.

Refer to Relationship of Direct & Indirect Costs with Fixed & Variable Costs to learn more.

Quite Good Guidance received