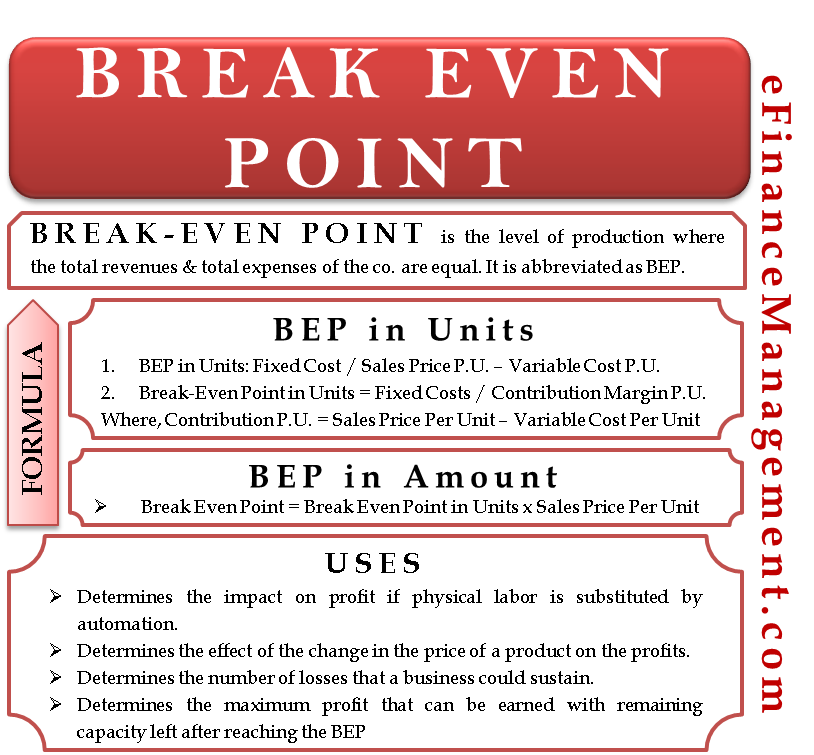

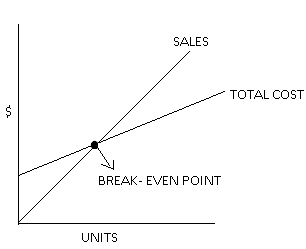

The Break-even point (BEP) is the level of production where the company’s total revenues and expenses are equal. At the BEP, the revenue of the company by the sale of manufactured products is equal to the total costs incurred in manufacturing the product. In accounting terms, at this point, the company’s total profit is zero. So it is a situation where there is no profit, no loss to the company.

Take an example for BEP; if the total revenues of ABC Ltd. are $ 7,000 and total expenses also equal $ 7,000, we can say that ABC Ltd. is working at the BEP.

The formula to calculate the break-even point in terms of the number of units is:

Break-Even Point in Units = Fixed Cost / (Sales Price Per Unit – Variable Cost Per Unit)

There is another simplified formula for calculating the BEP in terms of the number of units. That is,

Break-Even Point in Units = Fixed Costs / Contribution Margin Per Unit

Where,

Contribution Margin Per Unit = Sales Price Per Unit – Variable Cost Per Unit

Let us understand the meaning of contribution margin in brief. Contribution margin means revenue minus variable expenses. With contribution margin, you come to know how much of the company’s revenue will be available to pay for the fixed expenses and to generate the net income.

The formula for calculating BEP in value is:

Break-Even Point in Value = Break-Even Point in Units x Sales Price Per Unit

The Break-Even Point (BEP) in dollar value can also be calculated using the Contribution Margin Ratio. The Contribution Margin Ratio represents the percentage of each sales dollar that contributes towards covering the fixed costs and generating profit.

Break-Even Point in Value = Fixed Costs / Contribution Margin Ratio

Where,

Contribution Margin Ratio = (Price Per Unit – Variable Cost Per Unit) / Price Per Unit

Example

Calculate the BEP in terms of dollars and sales units from the information given below:

Fixed Cost: $ 10,000

Price Per Unit: $ 20

Variable Cost Per Unit: $ 10

Solution

Let us put the given information in the formula for calculating the BEP in terms of sales units:

Break-Even Point in Units = Fixed Costs / (Sales Price Per Unit – Variable Cost Per Unit)

= $10,000 / ($20 – $10)

= 1,000 units

Method 1

Break Even Point in Value = Break Even Point in Units x Sales Price Per Unit

= 1,000 x $ 20

= $ 20,000

Method 2

Here, I will calculate the Break-Even Point in terms of dollars using the Contribution Margin Ratio.

First, calculate the Contribution Margin Ratio:

Contribution Margin Ratio = (Price Per Unit – Variable Cost Per Unit) / Price Per Unit

= ($20 – $10) / $20

= 50% = 0.50

Break-Even Point in Value = Fixed Cost / Contribution Margin Ratio

= $10,000 / 0.50

= $20,000

The Break-Even Point (BEP) in terms of the value calculated using both methods should yield the same result.

Uses

The Break-Even Point (BEP) is a valuable financial tool that has several uses for businesses. Here are some common uses of the Break-Even Point:

Profitability Analysis

The Break-Even Point helps businesses assess their profitability by identifying the sales volume or revenue needed to cover all costs and achieve a net income of zero. It provides a baseline for understanding the minimum level of sales required to avoid losses and start generating profits.

Pricing Decisions

The BEP assists in determining optimal pricing strategies. By understanding the Break-Even Point, businesses can calculate the impact of different pricing scenarios on their profitability. It helps in finding the right balance between pricing, costs, and desired profit margins.

Cost Control and Efficiency

The Break-Even Point analysis encourages businesses to scrutinize their cost structure and identify areas where cost reduction and efficiency improvements are possible. By lowering fixed costs or decreasing variable costs, a company can lower its Break-Even Point and improve its financial health.

Sensitivity Analysis

The Break-Even Point can be used in sensitivity analysis to evaluate the impact of changes in variables such as costs, pricing, or sales volume on the company’s profitability. By assessing how variations in these factors affect the Break-Even Point, businesses can better understand their risk exposure and make strategic decisions to mitigate potential challenges.

The BEP serves as a reference point for financial planning and budgeting purposes. It helps businesses set realistic sales targets and revenue goals. By aligning their plans with the Break-Even Point, companies can develop more accurate budgets and forecast their financial performance.

Conclusion

Every business functions to earn profits. If it is unable to earn a profit, it aims to break even. BEP is a point where the revenues and expenses of a business are equal, and it is the next best position for a company that is not earning profits. It is the minimum point below which the company will start incurring losses, so the company’s management strives toward working above the BEP.

Quiz on Break-Even point.

Let’s review what you read here with a quick quiz test.

Sanjay Borad, Founder of eFinanceManagement, is a Management Consultant with 7 years of MNC experience and 11 years in Consultancy. He caters to clients with turnovers from 200 Million to 12,000 Million, including listed entities, and has vast industry experience in over 20 sectors. Additionally, he serves as a visiting faculty for Finance and Costing in MBA Colleges and CA, CMA Coaching Classes.

Concept clearly explianed. Nice??

Thanks. These ideas helps me a lot.