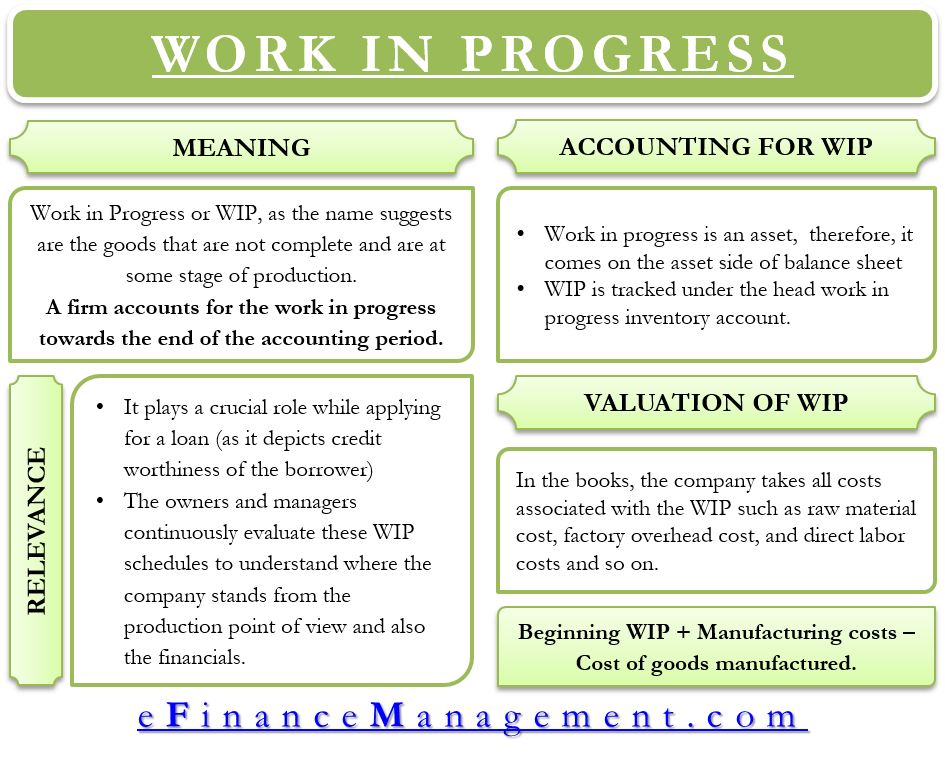

As the name suggests, work in progress, or WIP, are the goods that are not complete and are at some stage of production. The item is inclusive of entire raw materials that go into the production. It also includes the cost of processing. The cost of processing is significant because each semi-finish product moves through the various manufacturing steps.

A firm accounts for the work in progress towards the end of the accounting period. The accounting of WIP helps a company to determine the value of inventory that is in the production process.

Usually, there are three types of inventory:

- Raw material

- Work in Progress

- Finished Goods

Inventory of WIP is more valuable than the raw materials, which are yet to be put into manufacturing use. But, they are not more valuable than the finished goods. To put it simply, they are in the middle stage production process between the final product and the raw materials.

For instance, for producing a shirt, the fabric serves as the primary raw material. Then the company incurs labor costs in cutting and stitching the shirt. When the shirt is complete, the company transfers the total costs from WIP to the final inventory account.

Also Read: Capital Work in Progress (CWIP)

A term often used interchangeably with the WIP is the work in process. Though both terms mean the same, sometimes they may denote a different thing. The work in process may sometime refer to a product that moves from raw materials to a finished product in a short time, such as manufacturing goods. On the other hand, the work in progress may refer to an asset that needs more time for completion, such as construction or consulting projects.

Accounting of Work in Progress

Work in progress is an asset and must get the same treatment. Therefore, it comes on the asset side of the balance sheet, the same as raw materials or inventory. It is either a current asset or a long-term asset, depending on how the company uses it. Talking of the general ledger, the WIP is tracked under the head work in the progress inventory account.

Accountants either put the work in progress separately in the books or club it with other inventories. Clubbing it with other inventories is commonly done when work in progress is a small amount.

In the books, the company takes all costs associated with the WIP, such as raw material costs, factory overhead costs, direct labor costs, etc. While accounting for the WIP, the accounting manager will have to assign all the raw materials with the work project, compile related labor costs related to work done, record overhead costs, and after that, record the asset entry including all these costs.

Also Read: Types of Inventory / Stock

Importance of Work in Progress

One of the most reliable ways to keep an eye on the production capacity utilization of the company and production progress is to understand their WIP. Also, a company’s work-in-progress numbers play a crucial role when applying for a loan.

A point to note is that not many lenders would give a loan with the WIP as collateral since it will be difficult to sell WIP units in case a borrower defaults. Nevertheless, all external parties such as bankers, bonding agents, lenders, and underwriters evaluate work in progress to know the creditworthiness of the firm.

Also, both the owners and managers continuously evaluate these WIP schedules to understand where the company stands from the production point of view and also the financials. Therefore, a company must keep a close tab on the WIP and keep it up to date.

Valuing WIP

Arriving at an accurate WIP is a challenging process since there could be various WIP items at different production levels. To simplify the tasks, the companies wrap up their entire WIP items and transfer them to finish goods inventory before closing the books. Companies do this to ensure that there is no WIP to account for.

Alternatively, companies assign a standard percentage of the entire WIP items. This assumption considers that an average level of completion would be roughly correct when averaged over a large number of units.

It is possible to estimate the amount of ending WIP, but there is no guarantee on the accuracy of the result. The variations could be due to scrap levels, spoilage, rework, etc. Nevertheless, the formula for ending work in progress is:

Beginning WIP + Manufacturing costs – Cost of goods manufactured.

What is WIP Variance?

The variance occurs when there is a difference between the value of the completed goods report and reported the cost of production. Every company creates a single WIP account that keeps the record of all the production undergoing in a facility. This increases the challenge an accounting manager faces while assessing the WIP because production goes on consistently but reconciling at the same speed is not possible.

In order to streamline the process, reconciling at the order level is one of the methods that accounting managers commonly use. Arriving at the WIP value becomes easier once the production order is complete. Whatever cost a company incurs in the production for that order will appear as positive values. On the other hand, the value of goods that a company produces shows negative values. The net value of the total activities will be the variance for that production order.

Several factors lead to WIP variance, and most are due to human error. Therefore, reviewing WIP variance is a good point to start to close the gap between the actual and reported numbers. Moreover, small clerical mistakes could also result in big differences, and therefore, one must not ignore them.

Final Words

WIP is a crucial component for a company, and monitoring it will help keep the costs in check. Moreover, it is also a relevant item for the stakeholders. From the production point of view, however, companies nowadays are focusing more on reducing the number of WIP units in the production phase at a time. Doing this ensures a smoother production process and also reduces the defect rate. It also helps a company in minimizing the total investment in inventory.