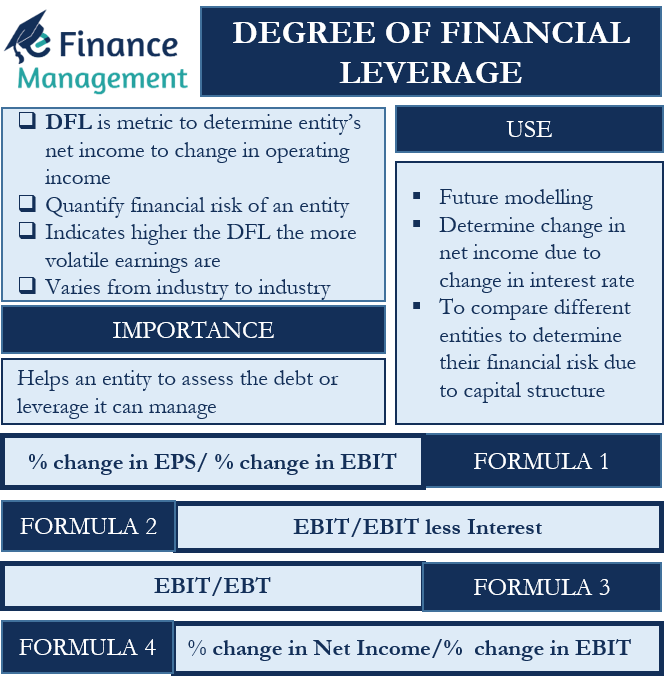

The degree of financial leverage or DFL is a type of leverage to determine the sensitivity of an entity’s net income to the change in the entity’s operating income. Generally, an entity with more debt and preference shares will have more financing costs, and thus, a change in its EBIT (earnings before interest and taxes) would have more impact on its net income. The reason is that the interest expenses and dividends on preference shares are fixed and permanent expenses. So, even if EBIT goes up, the interest on loans and preference share dividends will not go up proportionately. And this means net income would go up (and down) by a different percentage in line with the change in the operating income.

Since the change in the net income (EBT or earnings before tax) mainly results from the change in the capital structure, we can say that DLF determines the change in net income due to the change in the entity’s capital structure. DFL is one of the ways to quantify the financial risk of an entity. As a thumb rule the higher this ratio is the higher is the financial leverage enjoyed by the entity. And of course, that leads to higher volatility in the entity’s earnings.

DFL could vary drastically by industry and sector. Some industries can not operate without a high degree of financial leverage, such as airlines, retail stores, and more. These we call capital-intensive industries. On the other hand, some sectors operate with no or very less debt, such as software companies, and service sector entities.

Importance of Degree of Financial Leverage

As we understood the interest of debt remains a fixed expense and quantum thereof too. So, the use of debt or leverage could magnify returns and EPS when the operating income is growing. But at times when the operating income is dropping, taking on more financial leverage could prove problematic. And it will lead to a drastic drop in the EPS and earnings.

This is where DFL can help. It helps an entity to assess the debt or leverage it can manage comfortably and without affecting other operating parameters. As we discussed above if the operating income of the entity is stable then in all probability the earnings and EPS would also remain stable. This allows an entity to afford more debt. If the earnings of an entity are volatile, then it is advisable to keep debt within manageable levels.

Uses of Degree of Financial Leverage

Following are some of the popular uses of the degree of financial leverage:

- Since DFL helps find the changes in the net income based on changes in its operating income and capital structure, it is very useful for future modeling. For example, if a firm decides to use the DFL to take on more debt in the future, it would increase its interest expenses. This would result in a higher breakeven point as well.

- Apart from the interest expenses, DFL can also help determine the change in net income due to the change in the interest rate.

- One can also use DFL to compare different entities to determine the one with more financial risk due to their capital structure. Even investors can use this information to make investing decisions. For instance, investors can choose to invest in entities with higher financial risk during an expanding economy. This is because, during the period of economic growth, such entities are more likely to post higher profits. On the other end, the investors might prefer an entity with lesser DFL in times of uncertain economic situation.

The Formula for Degree of Financial Leverage

There are more than one ways to calculate the DFL. The method that one selects depends on the objective one wants to calculate the DFL for. For example, if an entity plans to take on debt but is unsure about it, it should use the net income to calculate the DFL.

And, if the objective is to determine the impact of the decision to take more leverage, then EPS (earnings per share) is an appropriate measure for the DFL.

Following are the different formulas to calculate the DFL:

DFL = Percentage change in earnings per share / Percentage change in earnings before interest and taxes (EBIT)

Or Percentage change in EPS/Percentage change in EBIT

Also, DFL = EBIT/EBIT less Interest

Or Percentage change in net income/Percentage change in EBIT

Or EBIT/EBT

The higher the DFL number, the higher will be the degree of financial risk. A higher DFL number could prove dangerous to the earnings if operating income drops and interest expenses remain the same.

Also Read: Leverage and its Types

Examples of Degree of Financial Leverage

Let us try to understand the calculation of DFL with a simple example below:

Suppose Company A has no debt and an EBIT of $40,000 in year 1. Since there is no debt, EBIT and earnings after taxes will be the same. So, the DFL will be 1. For the sake of simplicity, we are assuming a zero tax rate.

In year 2, however, Company A takes on debt for business expansion. This results in an interest expense of $20,000 and an EBIT of $70,000. The earnings after taxes will therefore be $50,000. So, the DFL, in this case, will be 1.4 ($70,000/$50,000). This means for a $1 change in earnings before taxes; there will be a 1.4x change in the EBIT.

Let us consider another (more complex) example to get a better understanding of the DFL concept:

Assume there are two almost identical firms, A and B. Firm A is all-equity, and B has a mix of debt and equity in its capital structure ($50 million loans at an interest rate of 10%). The EBIT of the two firms was $10 million in Year 1. For firm B, the profit before tax will be $5 million (after deducting interest expenses).

For Year 2, assume two scenarios. The first scenario is the EBIT of both firms increased by 50%, and the second is EBIT dropping by 50%.

So, in the positive growth scenario, the EBIT of both firms rises to $15 million, and in the negative growth scenario, EBIT drops to $5 million.

Now, we need to calculate pre-tax income, for which we need to determine the annual interest expense.

For firm A (all equity), pre-tax income and EBIT will be the same. But for firm B, the interest expense will be $5 million ($50 million × 10%). So, for firm B, pre-tax income will be $10 million in the positive growth scenario and $0 in the negative growth scenario.

Let us use the following formula here to calculate the DFL:

DFL = Percentage change in net income/Percentage change in EBIT

For firm A, the DFL in both scenarios will be 1 as its EBIT and EBT are the same. As it has no debt.

Similarly, for firm B, % change in net income in the positive growth scenario will be 100% [($10M – $5M)/$5M] and % change in EBIT will be 50% [($15M – $10M)/$10M]

For firm B % change in net income in negative growth scenario will be -100% [($0 – $5M)/$5M] and % change in EBIT will be -50% [($5M – $10M)/$10M]

So, DFL for firm B in the positive growth scenario will be:

= 100%/50% = 2x

And, in the negative growth scenario will be:

= -100%/-50% = -2x

So, we can see that when a firm witnesses a positive growth in EBIT, the financial leverage contributes more towards income growth (from 1x to 2x). But, in the case of negative EBIT growth, the impact is the opposite, i.e., financial leverage leads to bigger losses.

Thus, entities must be extremely careful when adding debt to their capital structure as it has the potential to magnify both favorable and unfavorable impacts. At the same time growth is also not possible without debt funding. Of course, maintaining a reasonable level is the best option.