Net Operating Income Approach to capital structure believes that the value of a firm is not affected by the change of debt component in the capital structure. It assumes that the benefit that a firm derives by infusion of debt is negated by the simultaneous increase in the required rate of return by the equity shareholders. With an increase in debt, the risk associated with the firm, mainly bankruptcy risk, also increases, and such a risk perception increases the expectations of the equity shareholders.

A company’s capital structure is a mix/ratio of debt and equity in the company’s mode of financing. This debt ratio in the capital structure is also known as financial leverage. Some companies prefer more debt, while others prefer more equity while financing their assets. The ultimate goal of a company is to maximize its market value and its profits. In the end, the question that stands in front is the relation between the capital structure and the value of a firm.

Read Capital Structure & its Theories to know more about what is capital structure and what are its different theories. Let us now look at the first approach.

There is one school of thought advocating the idea that increasing the debt component or the leverage of a company will increase the value of a firm. On the other hand, increasing the company’s leverage also increases the company’s risk. There are various capital structure theories that establish the relationship between financial leverage, the weighted average cost of capital, and the firm’s total value—one such theory is the Net Operating Income Approach.

Net Operating Income Approach (NOI Approach)

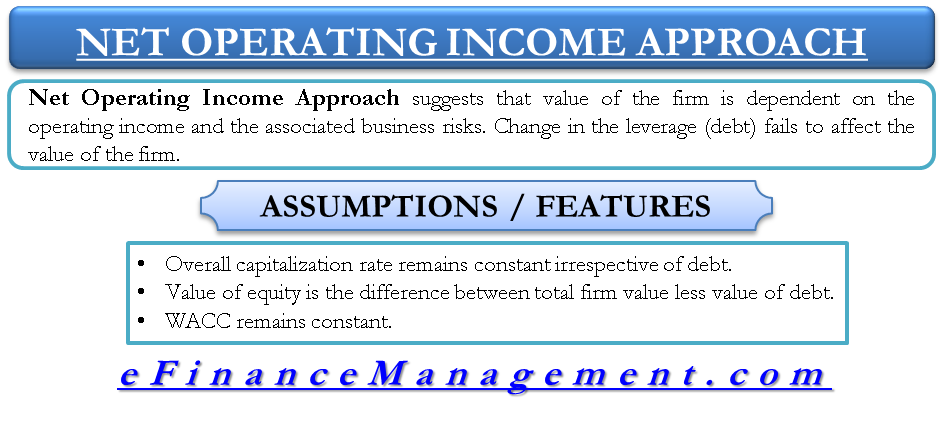

This approach was put forth by Durand and totally differs from the Net Income Approach. Also famous as the traditional approach, Net Operating Income Approach suggests that the change in debt of the firm/company or the change in leverage fails to affect the total value of the firm/company. As per this approach, the WACC and the total value of a company are independent of the company’s capital structure decision or financial leverage.

As per this approach, the market value is dependent on the operating income and the associated business risk of the firm. Both these factors cannot be impacted by financial leverage. Financial leverage can only impact the share of income earned by debt holders and equity holders but cannot impact the operating incomes of the firm. Therefore, a change in the debt to equity ratio cannot change the firm’s value.

It further says that with the increase in the debt component of a company, the company is faced with higher risk. To compensate for that, the equity shareholders expect more returns. Thus, with an increase in financial leverage, the cost of equity increases.

Assumptions / Features of Net Operating Income Approach

- The overall capitalization rate remains constant irrespective of the degree of leverage. At a given level of EBIT, the value of the firm would be “EBIT/Overall capitalization rate.”

- Value of equity is the difference between total firm value and less value of debt, i.e., Value of Equity = Total Value of the Firm – Value of Debt.

- WACC (Weightage Average Cost of Capital) remains constant, and with the increase in debt, the cost of equity increases. An increase in debt in the capital structure results in increased risk for shareholders. As compensation for investing in the highly leveraged company, the shareholders expect higher returns resulting in a higher cost of equity capital.

Diagrammatic representation of NOI Approach to Capital Structure

Example explaining Net Operating Income Approach to Capital Structure

Consider a fictitious company with the below figures. All figures in USD.

| Earnings before Interest Tax (EBIT) | = | 100,000 |

| Bonds (Debt part) | = | 300,000 |

| Cost of Bonds issued (Debt) | = | 10% |

| WACC | = | 12.5% |

Calculating the value of the company:

| (EBIT) | = | 100,000 |

| WACC | = | 12.5% |

| Market value of the company | = | EBIT/WACC |

| = | 100,000/12.5% | |

| = | 800,000 | |

| Total Debt | = | 300,000 |

| Total Equity | = | Total market value – total debt |

| = | 800,000-300,000 | |

| = | 500,000 | |

| Shareholders’ earnings | = | EBIT-interest on debt |

| = | 100,000-10% of 300,000 | |

| = | 70,000 | |

| Cost of equity | = | 70,000/500,000 |

| = | 14% |

Now, assume that the proportion of debt increases from 300,000 to 400,000, and everything else remains the same.

| (EBIT) | = | 100,000 |

| WACC | = | 12.5% |

| Market value of the company | = | EBIT/WACC |

| = | 100,000/12.5% | |

| = | 800,000 | |

| Total Debt | = | 400,000 |

| Total Equity | = | Total market value – total debt |

| = | 800,000-400,000 | |

| = | 400,000 | |

| Shareholders’ earnings | = | EBIT-interest on debt |

| = | 100,000-10% of 400,000 | |

| = | 60,000 | |

| Cost of equity | = | 60,000/400,000 |

| = | 15% |

As observed, in the case of the Net Operating Income approach, with the increase in debt proportion, the total market value of the company remains unchanged, but the cost of equity increases.

Also, read the Net Income (NI) vs. Net Operating Income (NOI) Approach.

very nice and simple, being a non commerce graduate student i understood this for my mba exam, keep ur efforts forever

well-done, indeed I’ve been exposed more on financial management. kudos .

This formula is the best but I understand another way. For this, I am simply satisfied with this.

Overall Thanks u Brother for your work.

Appreciated. Very easy to understand

Salute ? From: CA Student

God bless you

But in the calculation above, it should be 10,000,000 not 1000,000