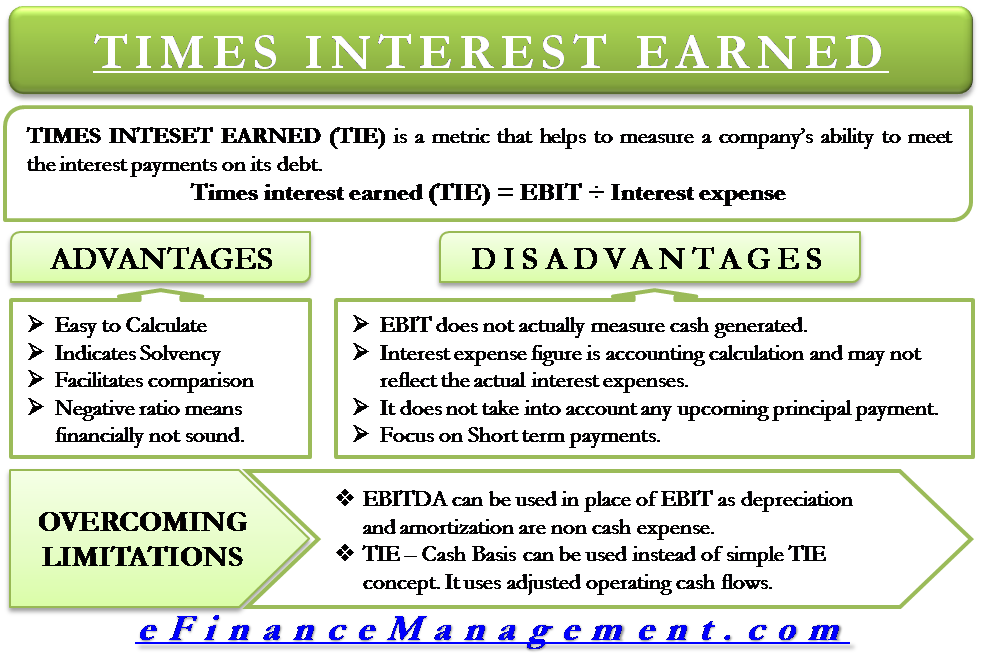

Times interest earned (TIE) is a metric that helps to measure a company’s ability to meet the interest payments on its debt. To calculate the TIE or interest coverage ratio, we use earnings before interest and taxes (EBIT) and the total interest payable, including bonds and other debts.

TIE indicates whether or not the company earns enough to cover its interest charges. Lenders mostly use it to ascertain if a prospective borrower can be given a loan or not.

Times interest earned is also considered by many to be a solvency ratio as it tells the ability of a firm to meet its interest and debt obligations. And, since the interest payments are for a long-term basis, the interest expenses are fixed expenses. If a company is unable to meet its interest expense, it may go bankrupt. And this is why TIE is seen as a solvency ratio.

Times interest earned is also known as Interest Service Coverage Ratio.

TIE Formula

Times interest earned (TIE) = Earnings before interest and taxes (EBIT) ÷ Interest expense.

Let’s understand TIE with the help of an example. Suppose a business has an EBIT of $100000 and interest payable on the loan is $25000. In this case, TIE will be 4 ($100000/$25000). This means the company earns four times the money that it needs to pay as interest.

Also Read: Interest Service Coverage Ratio

Higher TIE is good both for the lenders and borrowers. But, a usually big TIE could also mean that the company is “too safe” and is missing on productive opportunities. On the other hand, a TIE of lower than one indicates the company may not have sufficient funds to meet the debt obligation.

To know if the TIE of a company is “safe” or “too face,” or “low,” one must compare it with the companies operating in the same industry.

Advantages

- It is easy to calculate.

- The ratio indicates the solvency of a company.

- It can help to compare the two companies.

- A negative ratio means the company is not financially sound.

Limitations

- Using EBIT to calculate TIE does not give a clear picture. EBIT does not actually mean the cash generated by the business. It is possible that much of the sales of the business are on a credit basis. On the other hand, it may also happen that the ratio may come low even if the business has significant positive cash flows.

- The interest expense figure is also an accounting calculation and may not reflect the actual interest expenses. For instance, it may include a discount or premium on the sale of bonds. To avoid this, one should calculate the interest using the rate given on the face of the bonds.

- The metric does not take into account any upcoming principal payment. TIE may show a favorable number even if the business is facing a principal payment that is big enough to eat up all EBIT.

- It primarily focuses on the company’s short-term ability to meet the interest payment as it is based on the current earnings and expenses.

How to Overcome Limitations?

In place of EBIT, one may use EBITDA (earnings before interest, taxes, depreciation, and amortization) to get the real cash position. Depreciation and amortization are non-cash expenses, and thus, they don’t impact the cash position.

We could also use Times Interest Earned (Cash Basis) (TIE-CB) to get an even clearer picture. It is similar to the normal TIE, except that TIE-CB uses adjusted operating cash flow instead of EBIT. The ratio is calculated on a “cash basis” as it considers the actual cash that a business has to meet its debt obligations.

Also Read: Solvency Ratios

Also, an analyst should prepare a time series of the TIE to get a better understanding of the company’s financial standing. A single TIE may not be much helpful as it would include one-time revenue and earnings. So, calculating TIE regularly would give a better picture of a firm’s financial standing.