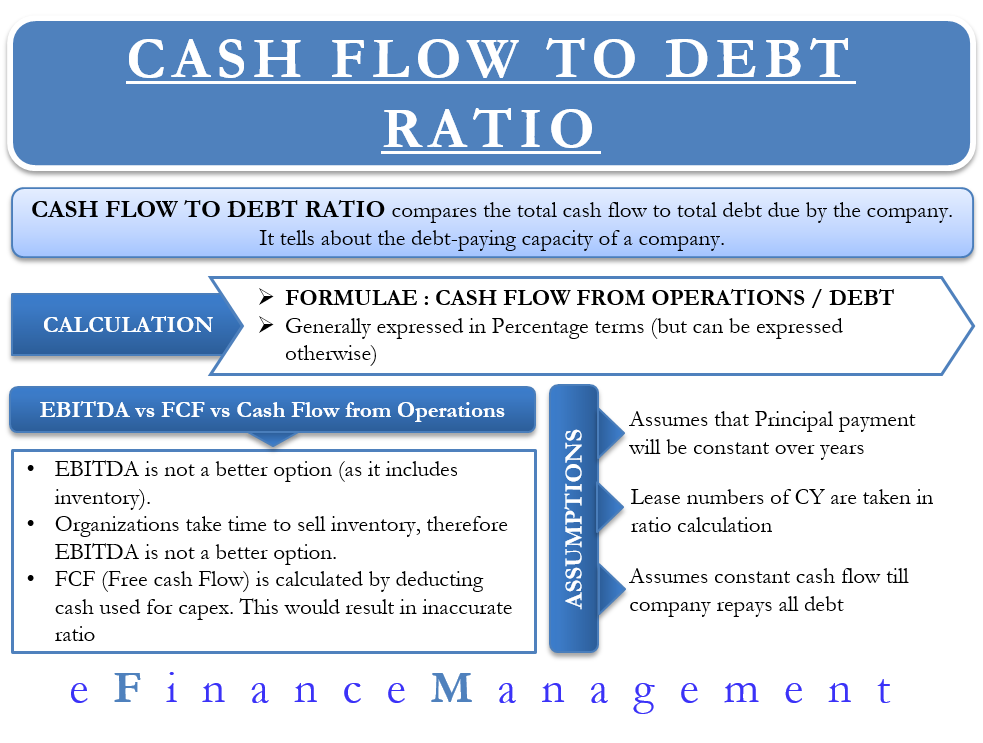

As the name suggests, the cash flow to debt ratio compares the total cash flow to the total debt due by the company. It is one of the coverage ratios used in the financial world to check the company’s health. The ratio tells about the debt-paying capacity of a company.

How To Calculate?

To calculate this ratio, we consider the cash flow from operations. Cash flow from operating activities is a better measure of a company’s strength than EBITDA (Earnings before Interest, Tax, Depreciation, and Amortization).

The formula for the Cashflow to Debt ratio is = Cash flow from operations/Total Debt.

The other name for this ratio is the Cash Flow Coverage Ratio.

We can get the operating cash flows from the cash flow statement while the debt amount is there on the company’s balance sheet.

For example, Company A has cash flow from operations is $25000, while its total debt is $100000. In this case, the ratio will be 25%. This means that if a company uses all its cash flow from operations to pay its debt, it will retire 25% of the total debt.

Mostly, this ratio is expressed as a percentage. However, if a company wants to show the number of years it would take to pay off all its debts, then one can present the same ratio in years as well.

Also Read: Cash Flow Coverage Ratio

For instance, the company’s cash flow to debt ratio is 25%. Then, the formula to convert it into years will be 1/0.25 = 4 years. This means that the company would roughly take four years to repay all its debt from the generated cash flow.

Can We Use EBITDA or FCF?

We may also use EBITDA in the formula in place of the cash flow from operations. However, it is not a better option because EBITDA includes the purchase of new inventory. Usually, organizations take some time to sell the new inventory and generate cash flow from it. Therefore, EBITDA would not accurately picture how much cash is available to the company to pay off its debts.

Analysts often prefer replacing cash flow from operations with free cash flow (FCF). Free cash flow is taken after deducting cash used for capital expenditures. Using free cash flow will affect the ratio and show the company as being less capable of servicing its debt. The result could also differ if an analyst chose either the long-term or short-term debt to calculate the ratio. The ratio would give better results if the analysts select short-term debt, but the company has more long-term debt on its balance sheet and vice versa.

Cash Flow to Debt Ratio – Assumptions

Does Not Cover Amortization

This ratio assumes that principal payments would not change and be consistent with the previous years. Although convenient to assume, this might not be the case in real-world scenarios. Over time, companies can avail various financial schemes that could include balloon payments, bullet payments, amortization, and so on. All these schemes result in the company paying massive interest in some years and none in other years.

Also Read: Cash Flow Coverage Ratio Calculator

Lease Increment

Lease numbers for the current year are taken into account while calculating the ratio. Usually, lease agreements come with a lease increase provision. But, the ratio does not reflect the same.

Constant Cash Flows

The ratio assumes that a company will earn the same cash flow in the future years, at least until the company repays the debt.

How Much is Enough?

Usually, companies aim for a cash flow to debt ratio of anywhere above 66%. The higher the percentage, the better the chances that the company would be able to service its debts. However, the ratio should neither be very high nor too low.

A high Cash flow to debt ratio would indicate two things:

First, the company is big enough and efficient to generate higher cash flows to service its debt. This could be true in the case of big companies in the industry. These companies might also have more favorable terms and conditions with the lenders, thereby having easy debt servicing agreements.

Second, there might be some companies that do not keep an acceptable debt portion in their books. Such companies would also have a good cash flow to debt ratio. However, investors might have a second thought while investing in such companies. These companies might be borrowing too little, which means they are losing on the higher returns.

To check if the ratio is too high or low, a financial analyst should consider a ratio in context with the company’s past performance. Or compare it with other companies in the same sector.

The cash flow to debt ratio for the current year would not give the true picture of the company’s overall performance. Therefore, tracking the ratio over the past four to five years could help understand how the company has improved or gotten worse with time in paying the debt.

Moreover, one can use the cash flow to debt ratio to compare companies in the same industry for their debt-servicing capacity. There are chances that capital-intensive industries may have a lower cash flow to debt ratio when compared to the other industries.

Please reconfirm the correctness of the cash flow figure ($25,000) and total debts figure ($10,000) used in above example. I think the company can repay its debt fully in year 1 except the total debts is $100,000.

Thanks for the suggestion, the required correction has been made. Thanks Again.