Advantages and Disadvantages of Profitability Ratios

The advantages and disadvantages of profitability ratios are important things to keep in mind before utilizing these ratios in analyzing a company. The ratio analysis is one of the important fundamental analysis tools. You can use it to judge whether the company is among the plausible investment category. You can do the ratio analysis of a company on a standalone basis or by comparing it with the industry peers. Among various categories, we will discuss today the pros and cons of profitability ratios. Profitability ratio as one of the categories has subcategories. Whenever you deal with profitability ratios, you always think of profits as a percentage of something. Let’s take some of the important ratios under this category that represent the entire profitability ratio category, and discuss the benefits and disadvantages of the same.

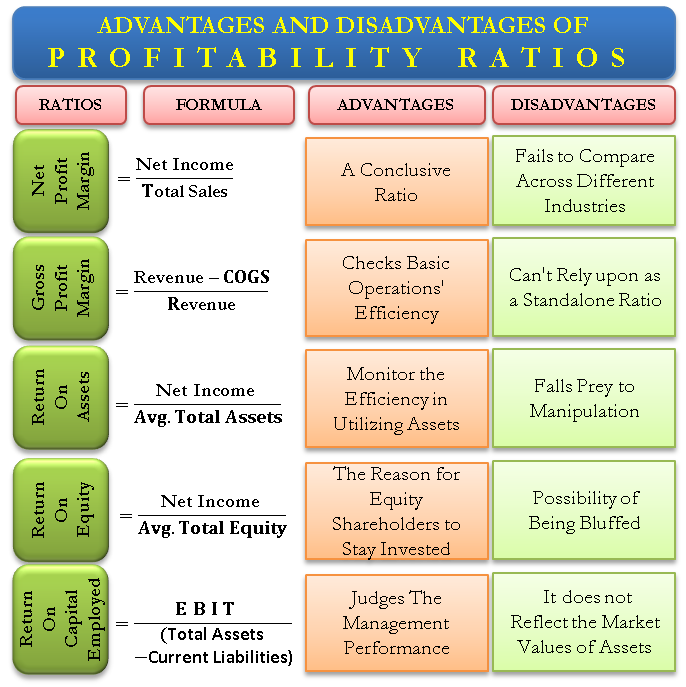

List of Important Profitability Ratios

- Net Profit Margin: Net Income/ Total Sales

- Gross Profit Margin: (Revenue – Cost of Goods Sold) / Revenue.

- Return on Assets: (Net Income) /(( Opening Assets at the beginning of the year +Closing Assets at the end of the year)/2).

- Returns on Equity: Net Income / ((Opening Equity at the beginning of the year + Closing Equity at the end of the year)/2).

- Return on Capital Employed: Earnings before Interest and Taxes / (Total Assets – Current Liabilities)

Advantages of Profitability Ratios

With the help of the ratios listed above, we will see the advantages of using profitability ratios for analyzing a company’s performance.

NP Margin – A Conclusive Ratio

First of all, the net profit margin (NP margin) is the most conclusive ratio for a business. Generally, if this ratio performs well in the current year and the trend is also growing, most likely, the company is on the right track. Why do we call it a conclusive ratio? It is because if there are major issues with other ratios or the company’s performance, it will impact this ratio. It is good to start the investigation or analysis by looking at this ratio.

GP Margin – Checks Basic Operations’ Efficiency

What does a 40% gross profit margin (GP margin) mean? It means the cost of goods sold consumes 60% of the company’s overall sales. 40% of the sales take care of general and administrative expenses and net profit. So, the higher this ratio, the higher the chances of improvement in net profit margins. The main advantage of this ratio is that it figures out if there is a problem in the company’s basic operations. If this margin is not sufficient to cover the administrative and other overheads, the net profit margin will be low or negative.

ROA – Monitor the Efficiency in Utilizing Assets

The advantage of using the return on assets (ROA) ratio is that the management can monitor and then control the utilization of assets. Why is the utilization of assets important? Efficient and effective utilization of assets has a direct impact on profitability. A company creates a positive leverage effect with efficient asset utilization by producing and selling more units against the same depreciation cost in the income statement.

Also Read: Profitability Ratios

Return on assets conveys how much net profit the company generates by every dollar of investment in assets. Increasing return on the asset can simply mean that management is making the best use of the assets and vice-versa.

ROE – Reason for Equity Shareholders to Stay Invested

As the net profit margin, the return on equity (ROE) is the most widely used ratio. The advantage of this ratio is that It is comparable across the company’s peer group. How much return do you generate for the equity investors is what matters for the equity investors. Are you generating beyond the minimum required rate of return? Calculation of this metric will answer your query. This metric is used in the calculation of residual income valuation. Residual income valuation is used in calculating the intrinsic value of equity. ROE greater than the required rate of return increases the intrinsic value of equity shareholders and thereby maximizes wealth.

ROCE – Judges the Management Performance

Return on capital employed (ROCE) lets you know about the management’s performance in putting capital to its most efficient use. With this metric, you can judge the management performance across different companies in a similar industry. At times, management compensations are based on attaining a set target of this particular metric. Even more, this metric can be compared with companies across different industries. The advantage of utilizing the ratio is that it judges the efficiency of the overall funds’ utilization of the company. It covers both types of capital, equity as well as debt.

Disadvantages of Profitability Ratios

Like nothing in the world is free of drawbacks, profitability ratios are not an exception. Let’s see the cons of using the profitability ratios.

NP Margin – Fails to Compare across Different Industries

Companies from different industries cannot be compared on the basis of net profit margin. E.g., the net profit margin of IBM Corporation is not comparable with the Starbucks Corporation. A decrease in net profit margin may not necessarily be bad. The company may want to increase its market share by reducing prices and sacrificing margins. The type of strategy the company adopts must also be taken into consideration. With this strategy, if the company is able to double the sales and achieve 1.4 times of increase in absolute profits in dollars, whether the decrease in net margin is worth it? You know the answer.

Also Read: Net Profit Margin or Ratio

GP Margin – Can’t Rely upon as a Standalone Ratio

The gross profit margin may not convey the story like the net profit margin. Unlike the net profit margin, the gross profit margin is not the final figure; if the sales, general, and administrative expenses take a toll on the gross profit margin. This metric cannot be compared with companies that belong to different industries. The disadvantage of this ratio is that we cannot interpret this ratio in isolation without having a look at the net profit margin.

ROA – Falls Prey to Manipulation

Companies can manipulate the return on assets metric by reducing the assets on the balance sheet. If you happen to compare the return on assets of 2 companies in the same industries, then the companies’ choice of depreciation should also be taken into account. E.g., If company A is following straight-line depreciation and company B, double declining balance method for depreciation. Company B will have a higher return on assets at the beginning than Company A and a lower return on assets in the end than company A. Therefore, the choice of depreciation greatly affects this metric.

ROE – Possibility of Being Bluffed

At times, companies manipulate return on equity by performing the buyback of equity shares. The buyback is a method wherein the company purchases its own shares at a premium to the market rate in order to address the undervalued equity of the company. Or, the company may wish to buy back the shares to provide capital appreciation instead of giving dividends. Since the shareholder’s equity reduces due to a buyback, the company’s return on equity increases. Please note, in this case, return on equity is increasing due to its decrease in the number of shares which decreases the shareholder’s equity. The return on equity is not increasing because of the value creation in the company, which should ideally be the case.

ROCE – Does not Reflect Market Values of Assets

First of all, a major drawback of return on capital employed is that it considers the book value of the assets in its calculations. The book value of the assets reduces either due to depreciation, or the book value may not reflect the market value. E.g., the book value of the land on the balance sheet may be $10000, but the actual market value may be $100,000. Therefore, you must look at aftermarket values while calculating this metric. And also, the book values which reduce due to the non-cash charge and depreciation.

To know more, refer to GROSS PROFIT PERCENTAGE.