A swaption is a combination of two words – swap and option. So, it is an option that allows the holder the right, but not an obligation, to enter into a swap. A swap could be of any financial item, but it is usually of the interest rate. The holder of the swaption contract needs to pay a premium to the issuer. The terms of the swaptions contract are pre-decided.

There are different types of swaps. We can classify swaption on the basis of what the holder gets and receive and on the basis of execution styles.

On the basis of the first classification, there are two types of swaptions – payer swaption and receiver swaption.

And, on the basis of execution styles, there are three types of swaptions – Bermudan swaption, European swaption, and American swaption.

There are very minute differences between all five types of swaptions. However, to better understand swaptions, it is crucial that you understand the differences among all five – Payer vs Receiver vs Bermudan vs European vs American Swaption.

Payer vs Receiver vs Bermudan vs European vs American Swaption – Differences

The following are the differences between Payer vs Receiver vs Bermudan vs European vs American Swaption. However, let us first understand the basic characteristics of all these swaptions:

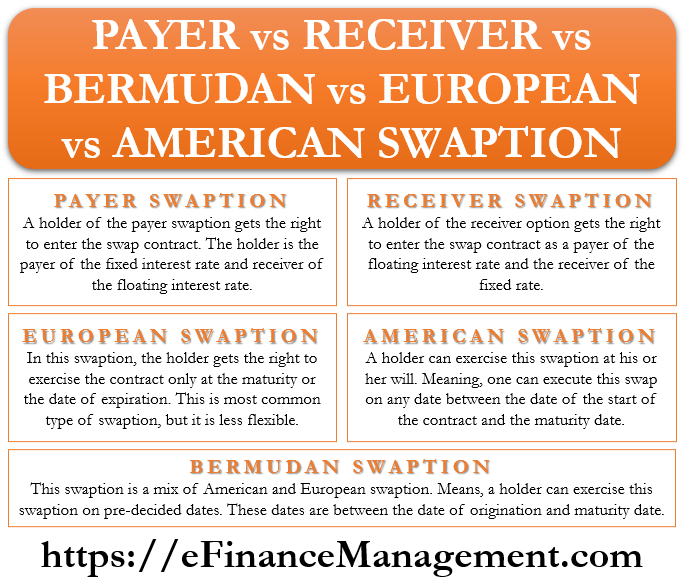

Payer Swaption

A holder of the payer swaption gets the right to enter the swap contract. The holder is the payer of the fixed interest rate and the receiver of the floating interest rate. The holder implements the contract if the fixed rate is more than the strike rate. We also call it a Put swaption.

Receiver Swaption

A holder of the receiver swaption gets the right to enter the swap contract as a payer of the floating interest rate and the receiver of the fixed rate. A holder, in this case, implements the swap contract if the fixed interest is lower than the strike rate. We also call it a Call Swaption.

European Swaption

In this swaption, the holder gets the right to exercise the contract only at the maturity or the date of expiration. This is the most common type of swaption, but it is less flexible for the holder. For example, if a European swaption has a maturity of 5 years, then the holder can exercise it only at maturity after five years. Talking about valuation, experts generally use the Black valuation model for valuing the European swaptions.

American Swaption

A holder can exercise this swaption at their will, which means that one can execute this swap on any date between the date of the start of the contract and the maturity date. Also, we can exercise this swaption on the maturity date as well.

For example, an American swaption has maturity after five years. This means the holder can exercise the swaptions on any day in five years. Thus, this type of swaption gives the holder more flexibility and freedom. There may be a small lockout period after the start of the swaption.

In comparison to the European swaption, American swaption is more complex to value. This is because of the freedom a holder gets in exercising this swaption. Generally, experts value American swaption using Black-Derman-Toy or Hull-White models. Or, one can also use two-factor stochastic methods and trinomial trees to value an American swaption.

Bermudan Swaption

This swaption is a mix of American and European swaption. This means a holder can exercise this swaption on pre-decided dates. These dates are between the date of origination and maturity date.

For example, a Bermudan swaption has a maturity of 5 years. The holder and issuer agree that the holder can exercise it on any one of the first four quarterly dates. This swaption is not as rigid as European swaption and not as flexible as the American swaption.

A Bermudan swaption is also more complex to value. So, like the American swaptions, experts use Black-Derman-Toy or Hull-White models to value Bermudan swaption.

Differences between Payer Vs. Receiver Swaption

| Payer Swaption | Receiver Swaption |

|---|---|

| The holder is the payer of the fixed interest rate | The option holder is the payer of the floating interest rate |

| The holder is the receiver of the floating interest rate | The holder is the receiver of the fixed rate |

| Holder implements contract if the fixed rate is more than the strike rate | Holder implements the swaptions if the fixed interest is lower than the strike rate |

| Another name for it is Put swaption | Another name for it is Call swaption |

Differences between European Vs. American Vs. Bermudan Swaption

| European Swaption | American Swaption | Bermudan Swaption |

|---|---|---|

| The holder can exercise the contract only at the maturity or the date of expiration. | The holder can exercise this swaption on any date between the date of the start of the contract and the maturity date. | A holder can exercise this swaption on mutually pre-decided dates |

| It is less flexible for the holder | This swaption gives the holder the utmost flexibility and freedom | This swaption is not as rigid as European swaption and not as flexible as the American swaption |

| Experts generally use the Black valuation model for valuing the European swaptions. | Experts value American swaption using Black-Derman-Toy or Hull-White models. | Here also, due to increased flexibility, the American swaption valuation techniques are used. |

| They are less complex to value | Most complex to value | Relatively less complex to value than American swaption |

Final Words

Despite minor differences between Payer vs Receiver vs Bermudan vs European vs American swaptions, all these swaptions are popular among investors. A point to note is that a Payer or Receiver swaptions can either be Bermudan or European or American Swaption. Similarly, a Bermudan, European, and American Swaption can either be Payer or Receiver.

It is to be noted that a swaption is a derivative terminology. It is basically an option or extension of any swap agreement. Though normally it is linked with interest rate swaps, however, there are many other types of swaps that are also traded in the market. These are like stock swaps, commodity swaps, currency swaps, etc.