Retained Earnings: Meaning

Retained earnings represent the cumulative profits earned by a company over time that have not been distributed as dividends to its shareholders. Instead, these earnings are reinvested back into the business, allowing it to finance operations, fund expansion projects, repay debts, or pursue other strategic initiatives. In simple terms, any extra profit that the company generates and is not paid to the shareholders is known as retained earnings. It is important to know how to calculate retained earnings to completely understand retained earnings.

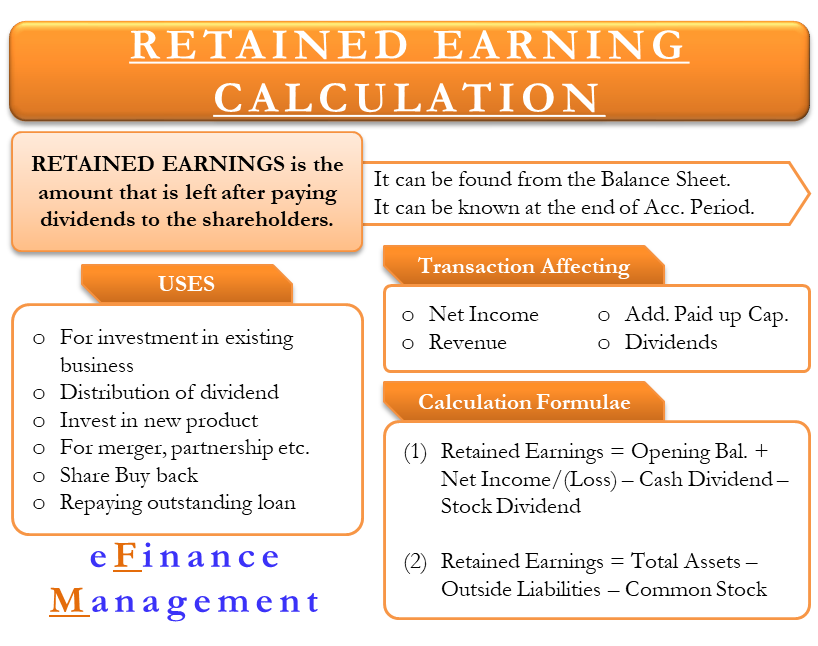

Uses of Retained Earnings

Companies usually deploy retained earnings for business development, which could be anything from expanding into a new product to a new market. Mostly the company use retained earnings for the following:

Business Expansion

Retained earnings are often used to finance expansion initiatives and facilitate business growth. Companies can reinvest these earnings in research and development, new product lines, geographical expansion, acquisitions, or capital expenditures. By using retained earnings for expansion, a company can avoid taking on additional debt or diluting shareholder ownership through external financing.

Dividend Payments

While retained earnings are primarily reinvested in the company, they can also be used to pay dividends to shareholders. Dividend payments are a way to distribute profits to investors, providing them with a return on their investment. However, the decision to pay dividends is at the discretion of the company’s management and depends on various factors, including financial performance, future growth prospects, and capital requirements.

Also Read: Statement of Retained Earnings

Share Buybacks

Retained earnings can be utilized for share buyback programs, where a company repurchases its own shares from the open market. By reducing the number of outstanding shares, share buybacks can increase earnings per share and enhance shareholder value. This strategy is often employed when a company believes its shares are undervalued or wants to return excess capital to shareholders.

Debt Reduction

Companies may choose to allocate retained earnings towards debt reduction. By paying down existing loans or obligations, a company can lower its interest expenses, improve its creditworthiness, and strengthen its balance sheet. Reduced debt levels can also enhance the company’s ability to secure favorable financing terms in the future.

Reserves and Contingency Funds

Retained earnings can be set aside as reserves or contingency funds to provide a financial cushion for unforeseen circumstances or future investments. These funds can be used to navigate economic downturns, industry-specific challenges, or to capitalize on strategic opportunities that may arise in the future.

How to Calculate Retained Earnings?

Before we detail how to calculate retained earnings, you must know where to find them in the financial statements and what items affect retained earnings.

Also Read: Retained Earnings Calculator

Where to Find Retained Earnings?

Retained earnings come in the company’s balance sheet under the shareholder’s equity section. A company usually prepares a balance sheet at the end of each accounting period. Therefore, retained earnings can only be known at the end of the accounting period.

Investors must know that retained earnings might not be just from the current year and may accumulate over the past several years. One can consider retained earnings as the company’s savings account in which the company deposits the surplus from all the years.

Transactions affecting Retained Earnings

Net Income

The amount for net income is part of the retained earnings. For those who are unaware, net income is the amount of profit that a company earns during a reporting period. To calculate it, one needs to subtract the cost of doing business from the revenue. Costs for the company can include operating expenses, utilities, rent, payroll, general and administrative costs, depreciation, interest on the debt, overhead costs, etc.

We call net income the bottom line as well because it is at the end of the income statement. If a company does not pay net income in the form of a dividend to the shareholders and instead retains it back, it is known as retained earnings.

In order to calculate the retained earnings for each accounting period, we add the opening balance of retained earnings to the net income or loss. From this amount, we will subtract the dividend payouts.

Retained Earnings (RE) = Beginning balance of the RE + Net Income/Loss – Cash Dividends – Stock Dividends

Dividends

A company can distribute dividends in the form of cash or stock. Both the forms lower the retained earnings value. A cash dividend reduces the cash balance and thus, reduces the size of the balance sheet and the overall asset value. In the case of stock dividends, there is no cash outflow. But, a portion of retained earnings reallocates from retained earnings to common stock and additional paid-in capital accounts. A point to note is that the overall size of the balance sheet remains the same in the case of a stock dividend.

Formula to Calculate Retained Earnings

Retained earnings might not always be a positive number as the company might earn a profit or lose revenue during a year. Similarly, a very large distribution of dividends to the shareholders might also be more than the retained earnings balance, resulting in a negative balance. Companies also maintain a summary report, known as the statement of retained earnings. This statement defines the changes in retained earnings for that specific period.

You can also use Retained Earnings Calculator for a quick calculation.

Example

Let us consider an example to better understand how to calculate retained earnings.

Company A has retained earnings of $10000 at the start of the year. For the year, Company A reported a net income of $5000 and paid $3000 as Dividends.

Now, retained earnings at the end of the year will be Beginning Balance + Net Income (or loss) – Dividends or $10000 +$5000 – $3000 = $12000.

Another Way to Calculate

The most common balance sheet relationship in accounting is between assets, liabilities, and stockholder equity. In the balance sheet, the company’s assets must be equal to the sum of the liabilities and stockholder equity.

Calculating retained earnings from the balance sheet is a two-step process;

First, subtract the liabilities from assets. The remaining balance will be stockholder equity.

Second, now look for the common stock line item on the balance sheet. Subtract the common stock from stockholder equity; what’s left will be the retained earnings.

This method assumes that the stockholder equity includes two items – common stock and retained earnings. Usually, companies with complex balance sheets also have additional line items and numbers.

RELATED POSTS

- Difference Between Retained Earnings and Reserves

- Retention Ratio – Definition, Calculation, Interpretation, Factors, and Limitation

- Statement of Stockholders Equity – Format, Example and More

- Contributed Capital vs Earned Capital – All You Need to Know

- Internal Sources of Finance

- Earnings Per Share