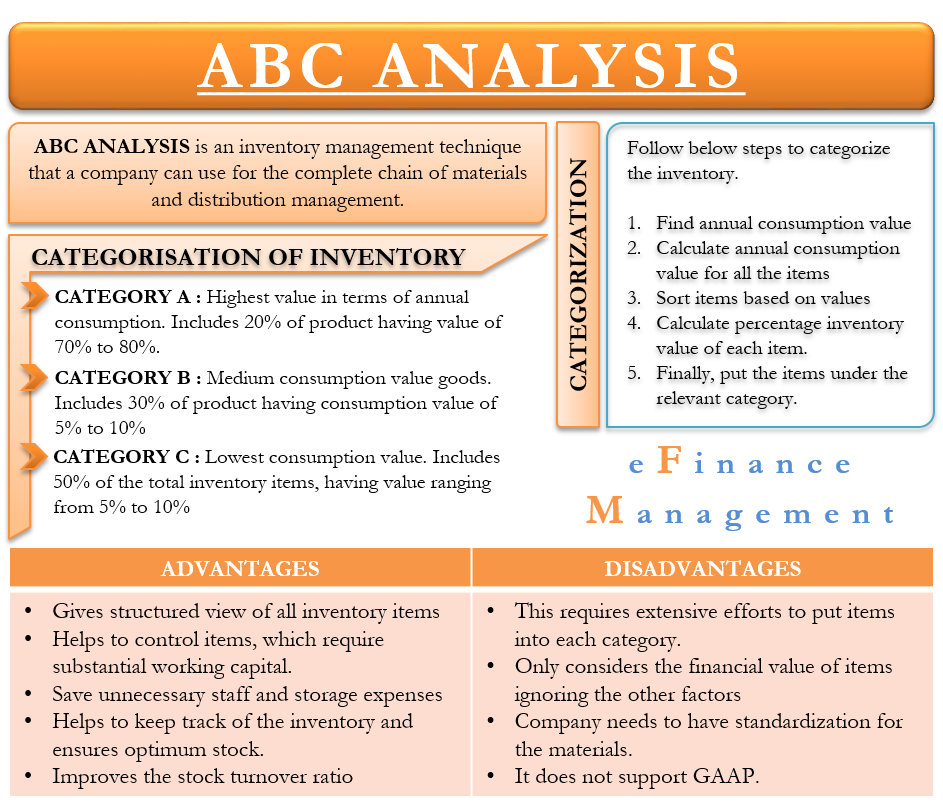

ABC Analysis is an inventory management technique that a company can use for the complete chain of materials and distribution management. In other words, we may also call it SIC (selective inventory control). Under this, the inventory is categorized into three categories, namely A, B, and C, based on their value.

Each of the three classes of inventory attracts a different level of management control. Therefore, this technique allows the management to distribute its focus by categorizing the inventory. As a result, more focus is on the goods of high value to them (under category A) and less on goods with low value (under C-category).

Such an inventory management technique seems to be based on the Pareto principle. As per this principle, the value of about 20% of the items accounts for 80% of the overall consumption value. In simple words, it means that 20% of the value of the products represents 80% of a company’s cost of raw materials.

This inventory management technique is applicable and useful for all types of products and raw materials and at every stage of production, whether it is at the unfinished stage, sub-assemblies level, or as spare parts, and more.

Also Read: Inventory Management Techniques

Categories Under ABC Analysis

Following are the three categories under which we divide all the goods under ABC Analysis:

Category A (70% Value 20% Volume)

Under this category, we take the goods with the highest value in terms of annual consumption. Usually, it is observed that about 15% to 20% of the inventory items by quantity represent the top 70% to 80% of the yearly consumption cost for a company. Thus, the A category includes about 20% of the products, which have an annual consumption value of 70 to 80%.

Category B (20% Value 30% Volume)

Items under this category have medium consumption value and are on the next priority list. These items are about 30% of the total inventory items by quantum and represent about 15% to 20% of annual consumption cost.

Category C (10% Value 50% Volume)

This segment has the items with the lowest consumption value, though they are the highest in terms of quantum. It forms about 50% of the total inventory items but only about 5% to 10% of the annual consumption value.

Note: we can easily calculate the annual consumption value of each product item using the formula – (Annual Requirements ) × ( cost per unit of the product).

Also Read: How EOQ helps in Inventory Management?

How does It work? – The Steps

Not every item in the inventory is of equal value. Some items will be more valuable than others. Similarly, some items come into use more frequently than others, and some items are both- high value and more use. With ABC inventory analysis, a company can determine the items that hold more importance and high value and hence, need more considerable attention.

To determine which items come under which category, we can use the following steps:

Firstly, we need to determine the annual consumption value. We can do this by multiplying the cost of the item by its annual consumption × item cost per unit.

Secondly, calculate the annual consumption value for all the items in the inventory.

Thirdly, sort the items based on their consumption value, from highest to lowest.

The fourth step is to calculate the percentage inventory value of each item. Use this formula – inventory value per item/sum of all inventory values.

Fifth, now put the items under the relevant category. For instance, the items accounting for the top 70-80% of the total inventory value will come under Category A. Similarly, items representing the next 15% will come under Category B. And the remaining items will come under Category C.

How to Treat Categories?

Now that we know how to put the items under each category, we must also know what different levels of treatment and attention each of these categories deserves. Our main objective should be to leverage this analysis. And don’t get lost or distracted by the volume of products. Instead, ensure due control and attention on critical and high-value items. And smooth availability of products to ensure uninterrupted production.

Treatment for Category A

- We need to follow strict inventory control and planning.

- Store these items in a highly secure area.

- These items need to be reordered regularly at set levels.

- The availability of these items helps to improve and better sales planning.

- Since these are essential items, a company must make sure that these items are never out-of-stock.

Treatment for Category B

- These are not as vital as those under A and not as insignificant as C.

- A regular robust inventory control system should be implemented for such items.

- A company must monitor these items for potential inclusion in the A category or to ensure they don’t fall into category C.

Treatment for Category C

- These are low-value and high-volume items.

- These do not need the level of security and monitoring as A category items.

- Its availability is easy, and supplier dependency is also low.

- A routine level of inventory system should suffice for these items.

- Management should explore alternate suppliers to improve the inventory carrying cost and quality.

Advantages

Following are the advantages of ABC Analysis:

- It gives the management a structured view of all the inventory items with their quantum and value.

- It allows the company to control items that require substantial working capital.

- Since it lowers focus on less essential items, it helps save unnecessary staff and storage expenses.

- It helps to keep track of the inventory and ensures optimum stock at all times.

- It helps improve the stock turnover ratio because of the systematic control of inventories.

- A company can maintain items in Category C without compromising on the relevant items.

- This inventory management technique helps with cycle counting systems. For instance, it helps the manager to decide the items to count once a quarter, or once every six months, or once in a year, and so on.

Disadvantages

Following are the disadvantage of this inventory management technique:

- This technique requires extensive efforts to put items into each category.

- It only considers the financial value of items, ignoring other factors that may be crucial to a company.

- To achieve the best results from this method, the company needs to have proper standardization for the materials.

- One major drawback of this system is that it does not support GAAP (Generally Accepted Accounting Principles requirements).

Final Words

ABC Analysis allows you to focus and manage your time and resources on the essential items. This, in turn, helps to save unnecessary staff and storage expenses. However, GAAP does not support this inventory technique. Therefore, companies using ABC analysis need a second costing system, one for the GAAP purpose, and others that work alongside the ABC method.

Also, read about other types of Inventory Management Techniques.