What is Debt to Equity Ratio?

Debt to equity ratio is a capital structure ratio that evaluates the long-term financial stability of a business using balance sheet data. We can also express it in terms of long-term debt and equity. Investors, creditors, management, government, etc., view this ratio from different angles influenced by their objectives. Therefore, the meaning and interpretation of this financial ratio vary with the objective with which it is looked at.

The debt-equity ratio, a renowned ratio in the financial markets, is defined as a ratio of debts to equity. It is often calculated to have an idea about the long-term financial solvency of a business. A business is said to be financially solvent until it can honor its obligations, such as interest payments, daily expenses, salaries, taxes, loan installments, etc.

How to Calculate Debt to Equity Ratio?

We need to use debts and shareholders’ capital to calculate the ratio. The formula for debt to equity ratio is as follows:

Simple Formula:

Debt to Equity Ratio = Debt / Equity

Detailed Formula:

This formula is a detailed bifurcation of each component of the numerator i.e. Debt and denominator i.e. Equity.

Debt to Equity Ratio = (Debentures + Long-term Liabilities + Short Term Liabilities) / (Shareholder’ Equity + Reserves and surplus + Retained Profits – Fictitious Assets – Accumulated Losses)

At first sight, the simple formula seems quite easy to calculate. It requires a good understanding of the terms, viz. debt, and equity. Both debt and equity are not a single item on a balance sheet, but they are broad term which includes many items. We have to ascertain the nature of different components of the balance sheet to decide their inclusion in the category.

Also Read: Debt Ratio

We have developed a Debt Equity Ratio Calculator for instantly calculating the ratio by plugging in the required figures in the formula.

Debts

In calculating the ratio, we define debt as the outside liabilities. As per the definition, the debt would include debentures, current liabilities, and loans from banks and financial institutions.

The inclusion of current liability is controversial because the debt-to-equity ratio is all about long-term financial solvency and current liability is a short-term liability. The amount of current liability fluctuates far and wide over the year. Further, current liabilities are taken care of in liquidity ratios (such as short-term and quick ratios), and their interest is not so huge. The other side of the coin demonstrates that, after all, the liability is an outside liability and holds similar preferential rights that get paid just like long-term debts in the event of liquidation. We all know that the number of current liabilities fluctuates in a year. This is true when looking at single items in the whole category, but a fixed portion of current liabilities always stays on the balance sheet.

Considering the explanation, we assume that the current liabilities should be part of calculating debts in the debt-to-equity ratio.

Equity

To calculate the debt-equity ratio, Equity should include equity shares, reserves, surplus, and retained profit, and subtract fictitious assets and accumulated losses.

The inclusion of preference share is debatable because nature is similar to debt as it creates a fixed obligation. Whereas inclusion is strengthened because it has ownership rights and does not possess the preferential right of payment like the debts have. Here again, the objective of calculating the ratio comes under the picture. Suppose the objective is to know the financial solvency. In that case, there should be an inclusion of preference capital in equity. In contrast, if the purpose is to evaluate the gearing effect of fixed dividends on earnings, it should be a part of the debt.

Example

Assume an entity has the following figures

| Debentures | 10000 |

| Long-term Liabilities | 15000 |

| Short-term Liabilities | 5000 |

| Shareholder’ Equity | 10000 |

| Reserves and surplus (R&S) | 25000 |

| Retained Profits | included in R&S |

| Fictitious Assets | 500 |

| Accumulated Losses | 0 |

Therefore, the debt-equity ratio will calculate as follows:

Debt Equity Ratio = (10000+15000+5000) / (10000+25000-500) = 30000/ 34500 = 0.87.

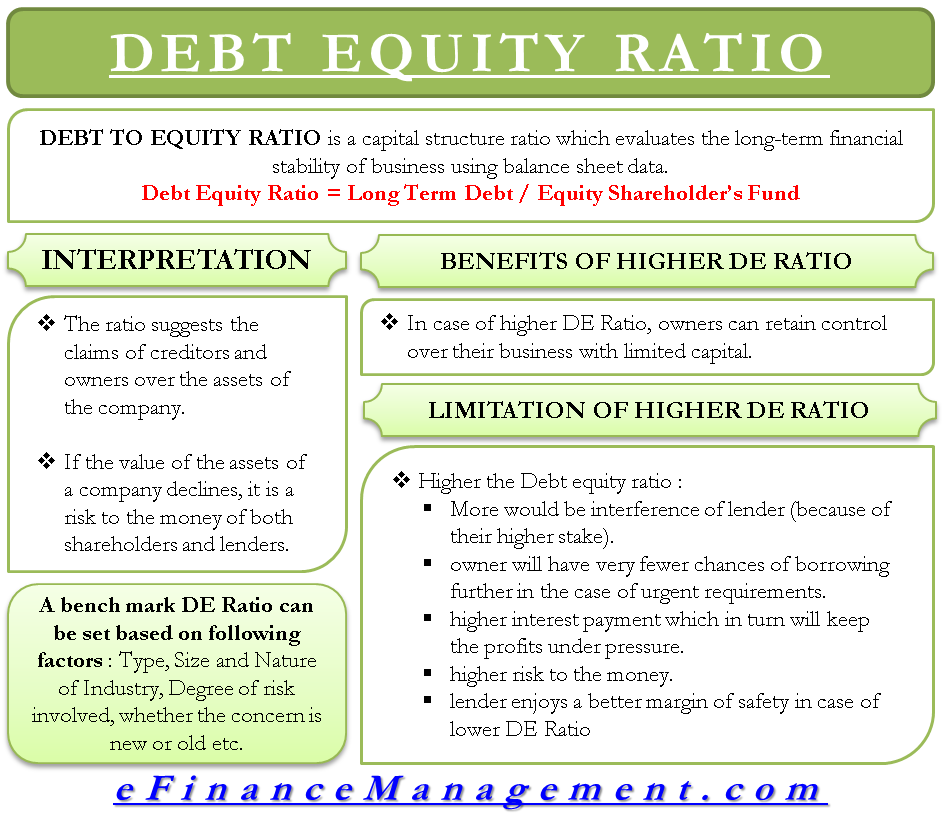

Interpretation of Debt to Equity Ratio

The ratio suggests the claims of creditors and owners over the company’s assets. Suppose the ratio comes to be 1:2; it says that for every 1 $ financed by debts, there are 2 $ being brought in by the equity shareholders. As we know, if the value of a company’s assets declines, it is a risk to the money of both shareholders and lenders. Since the lenders have preferential rights of payment, the risk would damage shareholders first and then reach lenders. The ratio of 1:2 suggests that if the asset value declines by 66.67%, it will not hamper the interests of the lenders. We also call it the margin of safety. If the ratio is 2:1, the margin is just 33.33%.

A higher debt-to-equity ratio indicates a higher proportion of debt financing relative to equity financing. It suggests that a company relies more on borrowing to finance its operations and growth. Conversely, a lower debt-to-equity ratio implies greater reliance on equity financing and signifies a more conservative capital structure.

Interpreting the debt-to-equity ratio requires considering the industry norms, company size, and the company’s specific circumstances. Industries with inherently higher capital requirements, such as manufacturing or utilities, tend to have higher debt-to-equity ratios compared to industries with lower capital needs, such as technology or service-based companies. Comparing a company’s debt-to-equity ratio with industry peers or historical data can provide a benchmark for evaluation.

The implications of the debt-equity ratio would be different for the firms and the lenders.

D/E Ratio for the Firm

Limitation of Higher D/E Ratio / Benefits of Lower D/E Ratio

- If the ratio is higher, the lenders will interfere in the management as they have a higher stake in the business.

- The owner will have fewer chances of borrowing further in the case of urgent requirements if the ratio is on the higher side, but we can manage the urgency well if the ratio is on the lower side.

- The Higher burden of interest will keep the profits under pressure.

Benefits of Higher D/E Ratio / Limitations of Lower D/E Ratio

The benefit for the owners is that they can retain control over their business with limited capital by preferring debts over equity. The owner can enjoy higher returns on equity because the total returns are divided into very few hands. Still, it is only possible when the rate of return from the business is higher than the rate of interest charged by the debts. This is called “Leverage” or “Trading on Equity.”

Visit Leverage Ratios for learning about more types.

D/E Ratio for the Lenders

A higher debt-equity ratio would mean a higher risk to the money. With a bit of stake in the business, the owners may not be very serious about the business. Any problem with the business will have a higher impact on lenders than on the equity shareholders. Here, the risk is high, but the returns are limited to interest. On the other hand, at a lower D/E ratio, the lenders enjoy a better margin of safety.

Benchmark Ratio

It is very difficult to state a benchmark debt-to-equity ratio since the usability of the ratio depends on many circumstances. Even from country to country, the practically acceptable norms vary. Apart from all the above, we should also consider the following circumstances :

- Type and size of the industry where the firm is operating.

- Nature of industry

- The degree of risk involved

- Whether the concerned borrower is a new or old business

Its beautifully explained and a tool to investors before investing in share market, its just like seeds selection by a farmer before planting in his fields for the yield, ratios and its interpretations help the investor, thanks for well explained, I am copying and trying to bring out the factors needed to layman ..’.the blind investors’ to know the abc of share market.